The paper summarized here is part of the Fall 2022 edition of the Brookings Papers on Economic Activity (BPEA), the leading conference series and journal in economics for timely, cutting-edge research about real-world policy issues. The conference draft of this paper was presented at the Fall 2022 BPEA conference. The final version was published in the Fall 2022 issue by Johns Hopkins University Press.

See the Fall 2022 BPEA event page to watch conference recordings and read conference drafts of all the papers from this edition. Submit a proposal to present at a future BPEA conference here.

Read final paper with comments, discussion summary and online appendix here»

Download data/programs for main paper here»

Download data/programs for Rognlie comment here»

People highly exposed to the economic consequences of the COVID-19 pandemic rapidly spent their federal Economic Impact Payments (EIPs) during the early months of the pandemic. However, many other people saved their payments, contributing to strong household balance sheets and, potentially, buying demand and price increases in the past year, suggests a paper discussed at the Brookings Papers on Economic Activity (BPEA) conference on September 8.

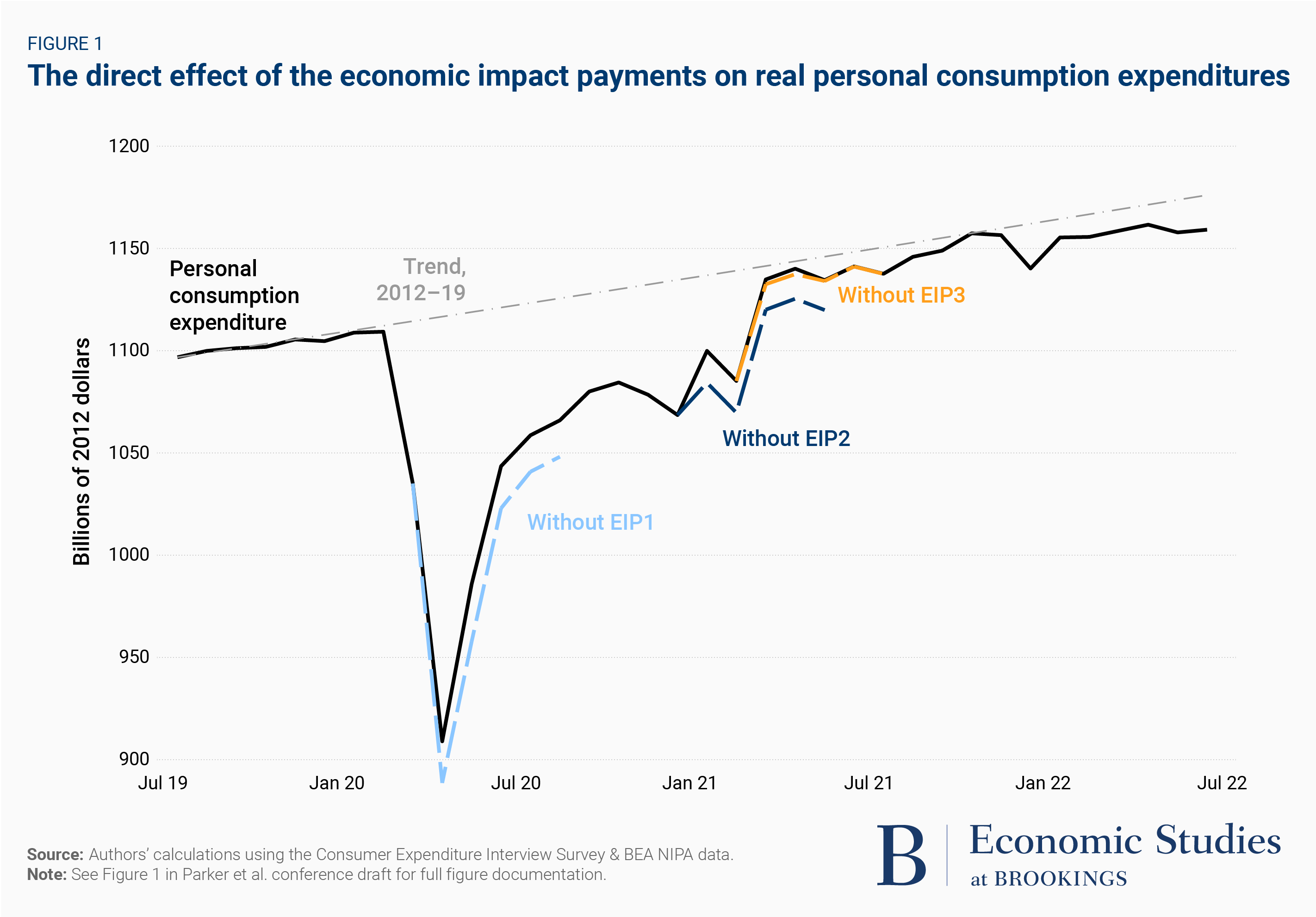

The authors—Jonathan A. Parker of the Massachusetts Institute of Technology, Jake Schild and Laura Erhard of the Bureau of Labor Statistics, and David S. Johnson of the University of Michigan—analyze the spending response to three rounds of payments approved by Congress in March 2020, December 2020, and March 2021.

In the first round, eligible households received $1,200 per adult and $500 per dependent child. In the second round (disbursed as the economy was recovering from its sharp slump early in 2020), households received $600 for each adult and child. And they received $1,400 per adult and dependent in the third round (when vaccines were starting to become widely available).

“From a demand management perspective, the unspent EIPs have contributed to strong household balance sheets over the past year, a period of strong demand and rising inflation.”

The payments came on top of two more-targeted programs: expanded unemployment insurance and the Paycheck Protection Program (aimed at keeping people employed at small- and mid-sized businesses). Moreover, income eligibility limits for payments were relatively high (for example, $150,000 for a married couple to receive a full payment), and the payments went to people whose income wasn’t hurt by the pandemic, such as retirees and people who could work from home.

Compared with tax rebates during previous economic downturns in 2001 and 2008, the increase in consumer spending generated by the payments was “substantively smaller”—especially during the second and possibly also the third round of payments, according to the paper, Economic Impact Payments and Household Spending During the Pandemic.

To measure the spending response, the authors use the monthly Consumer Expenditure Interview Survey, which the Labor Department uses to construct its Consumer Price Index (CPI). They note that, unlike during the 2001 and 2008 downturns (when mainly demand slumped), both supply and demand collapsed during the pandemic recession. However, even as shutdowns eased and vaccines became available, people apparently spent their payments only slowly or saved them as insurance against a potential future change in their economic circumstances, they write.

The third of households that were most economically exposed to the pandemic (people with low savings or who could not work from home) did consume substantially more rapidly out of the first round of EIPs, consistent with the payments providing pandemic insurance for some people, the authors note.

But they write: “From a demand management perspective, the unspent EIPs have contributed to strong household balance sheets over the past year, a period of strong demand and rising inflation.”

Together, the three rounds totaled roughly $850 billion. Meanwhile, CPI inflation in June hit a 40-year high of 9.1 percent from a year earlier before easing to 8.5 percent in July.

“While some households needed the payments to cover economic losses early in the pandemic, the fact that on average people spent little of their first payments suggests that a better-targeted policy could have been more efficient in that it could have provided more pandemic insurance at lower cost and without as much excess demand later,” Parker said in an interview with The Brookings Institution.

Citations

Parker, Jonathan A., Jake Schild, Laura Erhard, and David S. Johnson. 2022. “Economic Impact Payments and Household Spending during the Pandemic.” Brookings Papers on Economic Activity, Fall. 81-130.

Dynan, Karen. 2022. “Comment on ‘Economic Impact Payments and Household Spending during the Pandemic’.” Brookings Papers on Economic Activity, Fall. 131-138.

Rognlie, Matthew. 2022. “Comment on ‘Economic Impact Payments and Household Spending during the Pandemic’.” Brookings Papers on Economic Activity, Fall. 138-151.

Authors

Discussants

-

Acknowledgements and disclosures

Laura Erhard and Jake Schild are employees of the Bureau of Labor Statistics (BLS). BLS reviewed the research to ensure that the paper does not take a political stance and that it has correctly and accurately described and analyzed the consumer expenditure data that the BLS produces and releases to the public. The authors did not receive financial support from any firm or person for this paper or from any firm or person with a financial or political interest in this paper. The authors are not currently an officer, director, or board member of any organization with a financial or political interest in this paper. David Skidmore authored the summary language for this paper. Becca Portman assisted with data visualization.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).