Through the course of the pandemic, we have investigated the disproportionate pandemic impacts on U.S. families. In June, we reported that Black and Hispanic Americans faced higher rates of housing hardship than white Americans, and we emphasized the importance of identifying a long-term rather than a “Band-Aid” solution. In November, we found that housing inequality had gotten worse as the COVID-19 pandemic stretched onward. Now, almost a year after the pandemic’s onset, with COVID-19 vaccines distributed, we explore how housing inequality has changed over the course of the pandemic. Over the recent months, we find that the disproportionate experiences of housing hardship have lessened, but only because everyone became worse off. We also observe that Black families have become “long-haulers” when it comes to their experience of housing hardship.

Both housing-related hardship experiences and related inequality have been alleviated

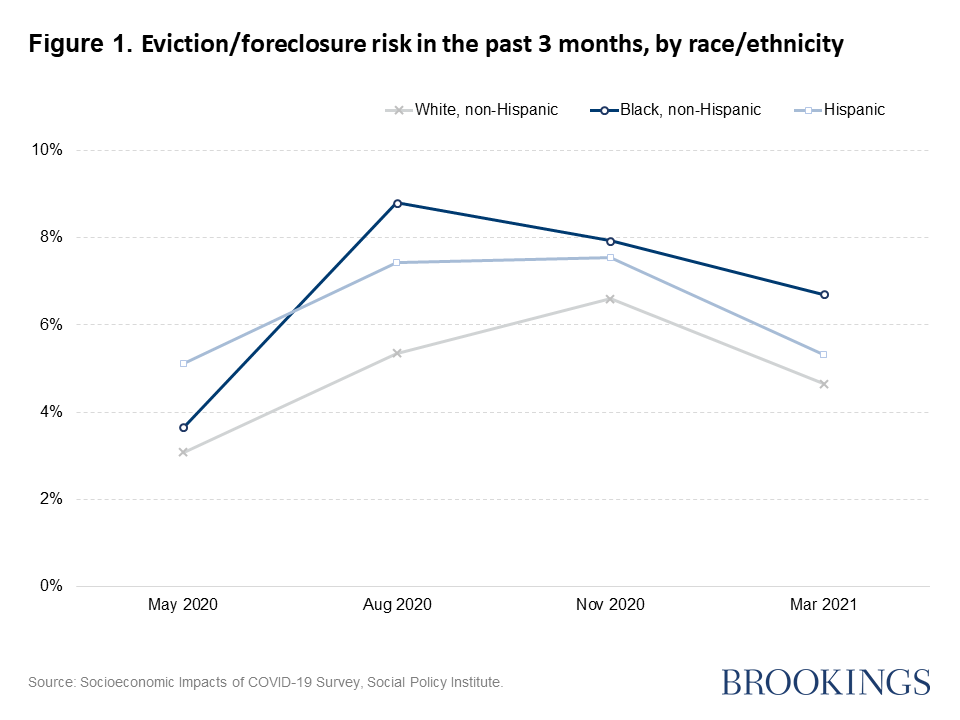

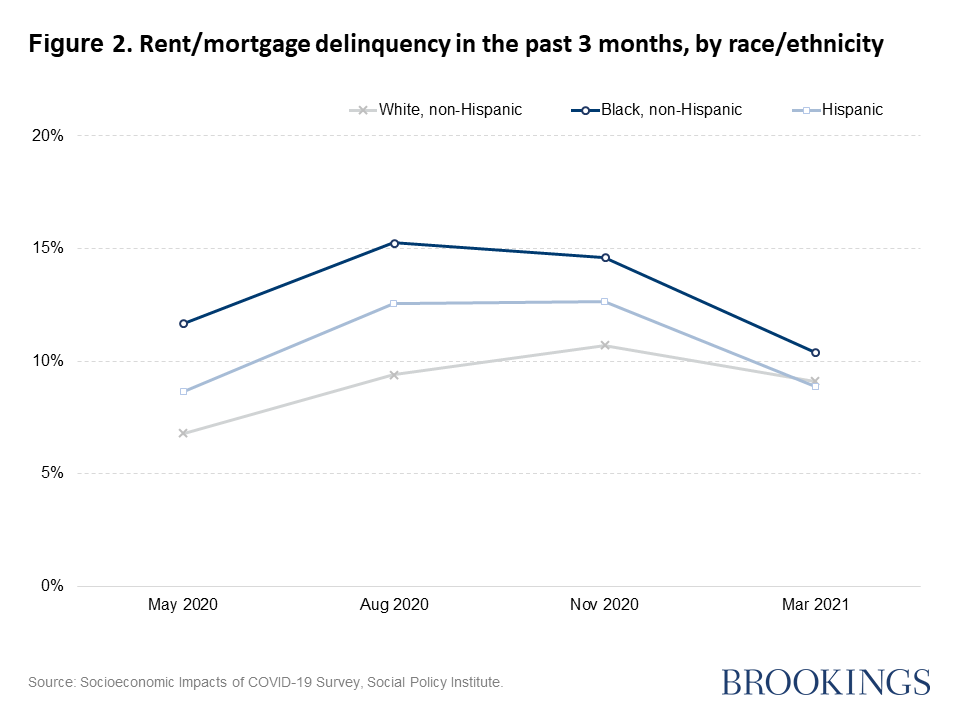

We first explore how housing-related hardship experiences have changed through the pandemic with respect to eviction/foreclosure (Figure 1), rent/mortgage payment delay (Figure 2), and utility bill payment delay (Figure 3). As previously reported, housing inequality worsened during the first six months after the pandemic. As of June 2020, 9 percent of Black and 7 percent of Hispanic respondents had experienced eviction/foreclosure, which was significantly higher than white respondents (5 percent) even after controlling for demographic and socioeconomic attributes. Likewise, in the same period, minority respondents were significantly more likely to experience rent/mortgage and utility payment delays compared to white respondents—rent/mortgage: 15 percent (Black), 13 percent (Hispanic), and 9 percent (white); Utility: 21 percent (Black), 20 percent (Hispanic), and 14 percent (white).

Housing inequality has since declined after its peak in August. This trend is, however, not because minority groups’ housing situations have become significantly more stable. Instead, white respondents are increasingly experiencing housing instability. For instance, between August and November, the eviction/foreclosure risks for Black and Hispanic respondents decreased by less than 10 percent (from an eviction rate of 8.8 percent to 7.9 percent for Black respondents and from 7.4 percent to 7.5 percent for Hispanic respondents). In the same period, however, white respondents’ eviction/foreclosure risk increased by 23 percent (from an eviction rate of 5.3 percent to 6.6 percent). Similarly, in November, we observe reduced inequality gaps in delayed payment of rent/mortgage and utility bills mainly due to the delayed peak of white respondents. The outlooks are becoming positive however, as we observe that both housing instability levels and inequality have decreased in March and April of 2021 compared to the previous survey in November 2020.

Black families have been more likely to be housing hardship long-haulers

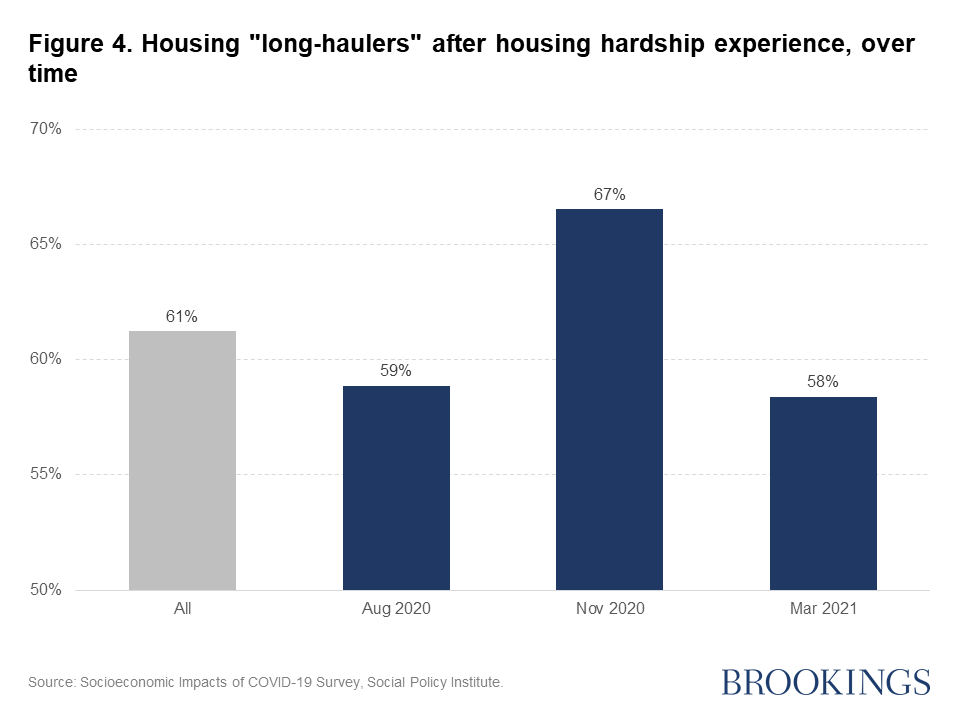

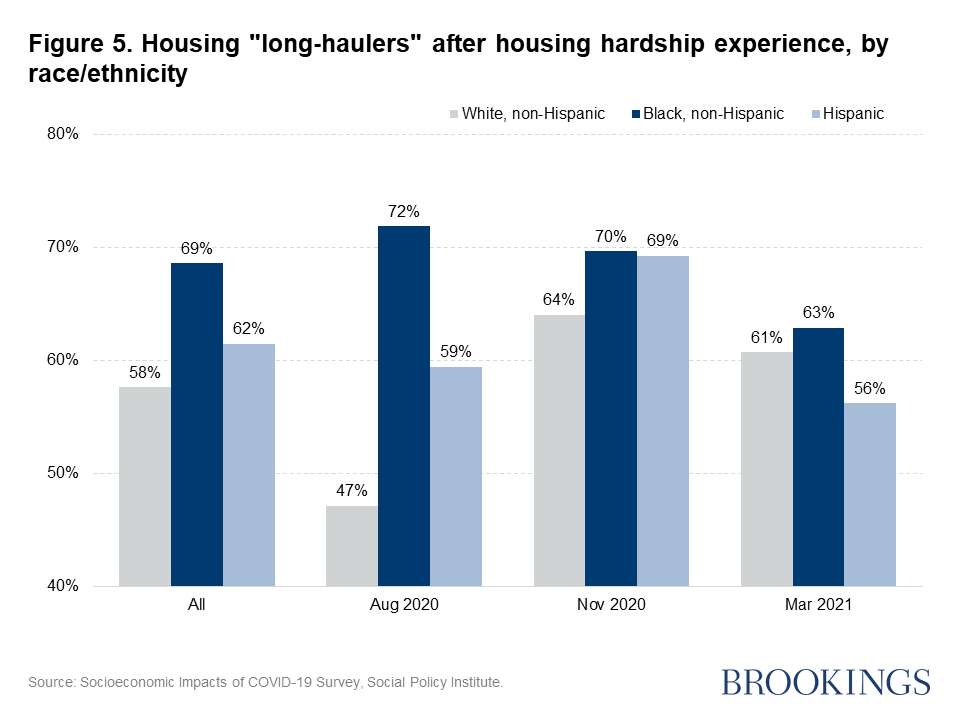

In addition to the housing instability, we also explore the incidence of housing hardships and how households have experienced differences in prolonged hardship by race and ethnicity. Similarly to the way the physical symptoms of COVID-19 can stay with the body and lead some individuals to become COVID-19 “long-haulers,” housing hardship has stayed with some households from one survey wave to the next. We looked specifically at families who experienced housing hardships (i.e., eviction/foreclosure, delayed rent/mortgage payments, and delayed utility bill payments) during the previous survey (three months prior to the present survey) and estimated how many of them still experienced these hardships three months later. For robust estimations, we controlled for both demographic and socioeconomic attributes.

Figure 4 reports how the incidence of living as a housing hardship long-hauler changed over the course of the pandemic. Of all respondents, 61 percent experienced housing hardship long-hauling at some time during the pandemic. This means that at two consecutive survey dates (each three months apart from each other) they reported experiencing housing hardship within the prior three months. In November, the proportion of long-haulers peaked with over two-thirds of respondents reporting that they had experienced housing hardship through at least two survey periods. Figure 5 deconstructs the proportion of housing hardship long-haulers by race/ethnic groups. Throughout the pandemic, Black respondents (69 percent) have more commonly endured housing hardship long-hauling than white and Hispanic respondents (58 percent and 62 percent respectively). This discrepancy was particularly pronounced at the beginning of the pandemic. In August, Black respondents were 1.5 times more likely than white respondents to keep experiencing housing hardships for two consecutive survey periods, this gap being statistically significant at p<.01 even after keeping other socioeconomic factors constant. However, similarly to the previous analysis, this disparity lessened in November due to more white respondents becoming housing hardship long-haulers.

Conclusion

Through a year of surveys, we’ve learned that minority groups, especially Black families, have been much vulnerable to the pandemic’s shocks. However, we also observe that hardships on minority families have been soon transmitted to everyone, including white households. Similarly, while a greater proportion of Black households are housing hardship long-haulers, more Hispanic and white households have joined that group in experiencing the long-term impacts of COVID-19 on their financial and residential stability.

Lingering housing hardship demonstrates the continued need for relief for both renters and homeowners with mortgages. The shrinking inequities between households of different races coupled with the slow crawl toward recovery shows that widespread financial relief is still needed across the country. Economic impact payments would be of little help, particularly for housing hardships long haulers who are already a couple of months behind in housing/utility bill payments. Rather, as our previous blog claimed, more proactive and sustainable remedies, such as a universal housing voucher, are needed.

Some people may argue that such proactive remedies are too expensive. For instance, the Congressional Budget Office estimated in 2015 that it would cost an additional $29 billion if the housing voucher were to cover those earning 30 percent of area median income (AMI) or less. Yet, infection and eviction are interlinked. Even though the expenditure seems huge, the cost of infections far outweighs the cost of supporting housing. Throughout the pandemic, social distancing has been key to minimizing COVID-19’s impacts by reducing the frequency and duration of contact individuals have with one another. The most powerful and effective way to keep social distancing is, obviously, to have people stay home.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Inequalities in housing hardship declined because everybody is now worse off

April 30, 2021