The price cap on Russian oil and refined products, conceived and implemented in the wake of Russia’s February 2022 invasion of Ukraine, was a novel attempt to reduce revenue from oil exports while maintaining global price stability. Successful application of the cap demands continued attention by the price cap coalition to sanction private entities that violate its terms. A particularly relevant issue today is whether further enforcement actions can dissuade Russia from utilizing an expanded “shadow fleet” to circumvent the terms of the price cap—and whether more aggressive sanctions enforcement will surge the price of oil. In this note, we argue that the coalition should sanction 15 Sovcomflot tankers that are especially active, shutting them down as a means of transport for Russia’s oil trade. Historical experience suggests that this enforcement measure is unlikely to have even a modest impact on global oil prices.

Background and context on the price cap

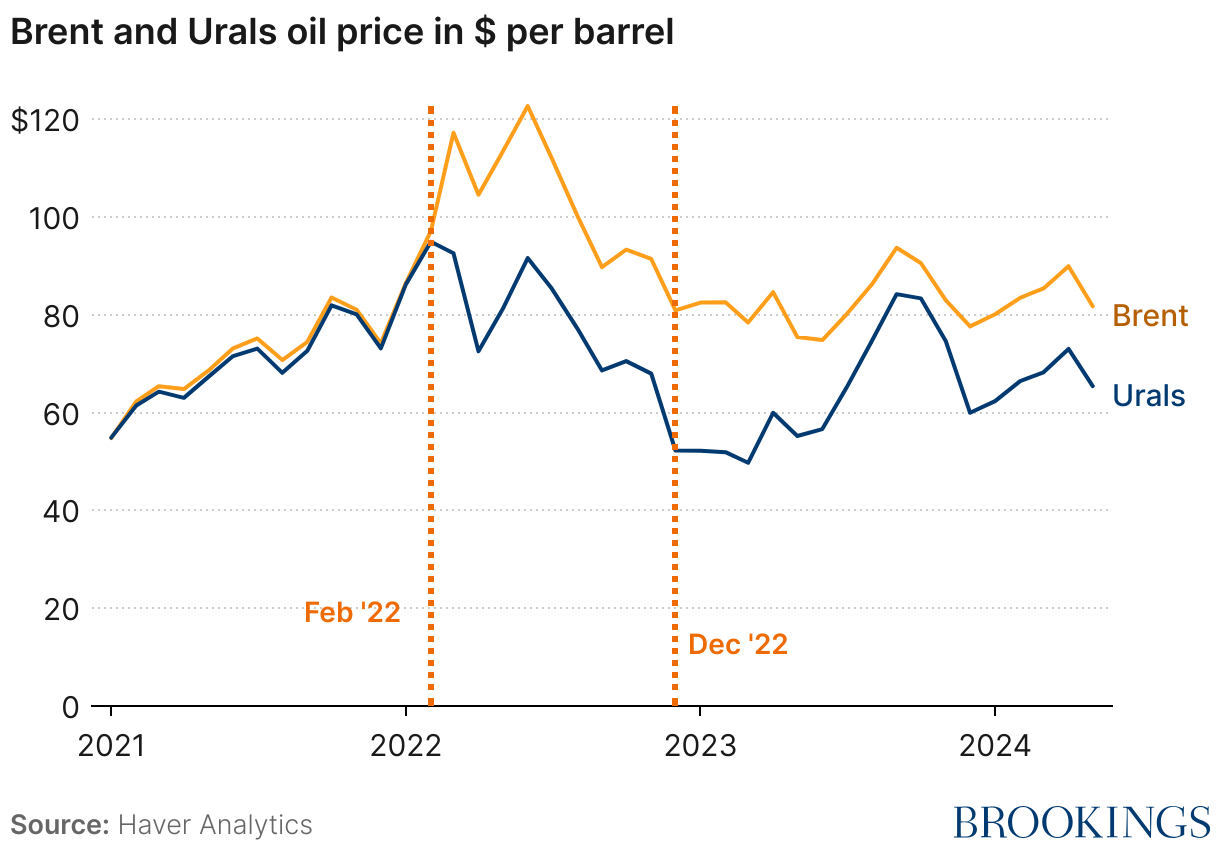

Russia is an important supplier of oil and refined products to the global economy. In the run-up to its invasion of Ukraine, Russia’s seaborne exports of crude and refined products were just shy of six million barrels per day, with a substantial share of these exports going to the European Union (EU) and other advanced economies. Before the invasion, the global benchmark price for oil—Brent—was very close to the price of Urals oil, which is the main reference blend for Russian crude sold on Baltic and Black Sea ports. The invasion changed that. Global oil prices spiked on fears of supply disruptions and a large discount on Urals versus Brent emerged as buyers shunned Russian oil (Figure 1). Yet, despite the unprecedented discount on Russian oil, revenues flowing to the Russian state rose to distressingly high levels.

In light of soaring Russian revenues and continued aggression towards Ukraine, the EU formulated a package of additional sanctions against Russia in the summer of 2022. This set of actions—the “sixth sanctions package”—aimed to both limit the EU’s import of Russian oil while also banning the use of European services in the Russian oil trade. The centrality of European services to the trade of Russian oil was tantamount to an embargo, which threatened to sharply raise global energy prices. Concerns about an oil price shock led Ukrainian allies to consider a price cap on Russian oil in lieu of an outright services ban.

The price cap was established with the dual goals of limiting Russian profits from the trade of crude oil and refined products while also maintaining stability in global energy markets. The central approach established by the price cap coalition (the G7, plus the European Union and Australia) was to disallow the provision of services in trades that exceeded the maximum allowable price of each product. The primary lever utilized by the coalition was the sanctioning of service providers who violated these terms, with a broad range of services subject to the cap, including shipping, insurance, brokering, flagging, and financing.

The success of the price cap was most pronounced in the early stages of its implementation, especially in terms of limiting trading profits accruing to Russia. In terms of export volumes, Russia’s seaborne exports of crude oil and refined product have been stable near six million barrels per day since December 2022, so a key goal of the price cap—to ensure the continued flow of Russian oil to global markets—has been met. Simultaneously, the composition of its exports has shifted away from advanced economies—which now import near zero—to emerging markets, where China, India and Turkey have emerged as large buyers. Despite drastic reshuffling of its export destinations, export volumes have remained largely stable since the invasion of Ukraine—and have even increased on the margin prior to recent voluntary cutbacks to meet OPEC+ production quotas. Price stability has accompanied global production stability, which is somewhat remarkable when contrasted against geopolitical turmoil in oil production-relevant regions.

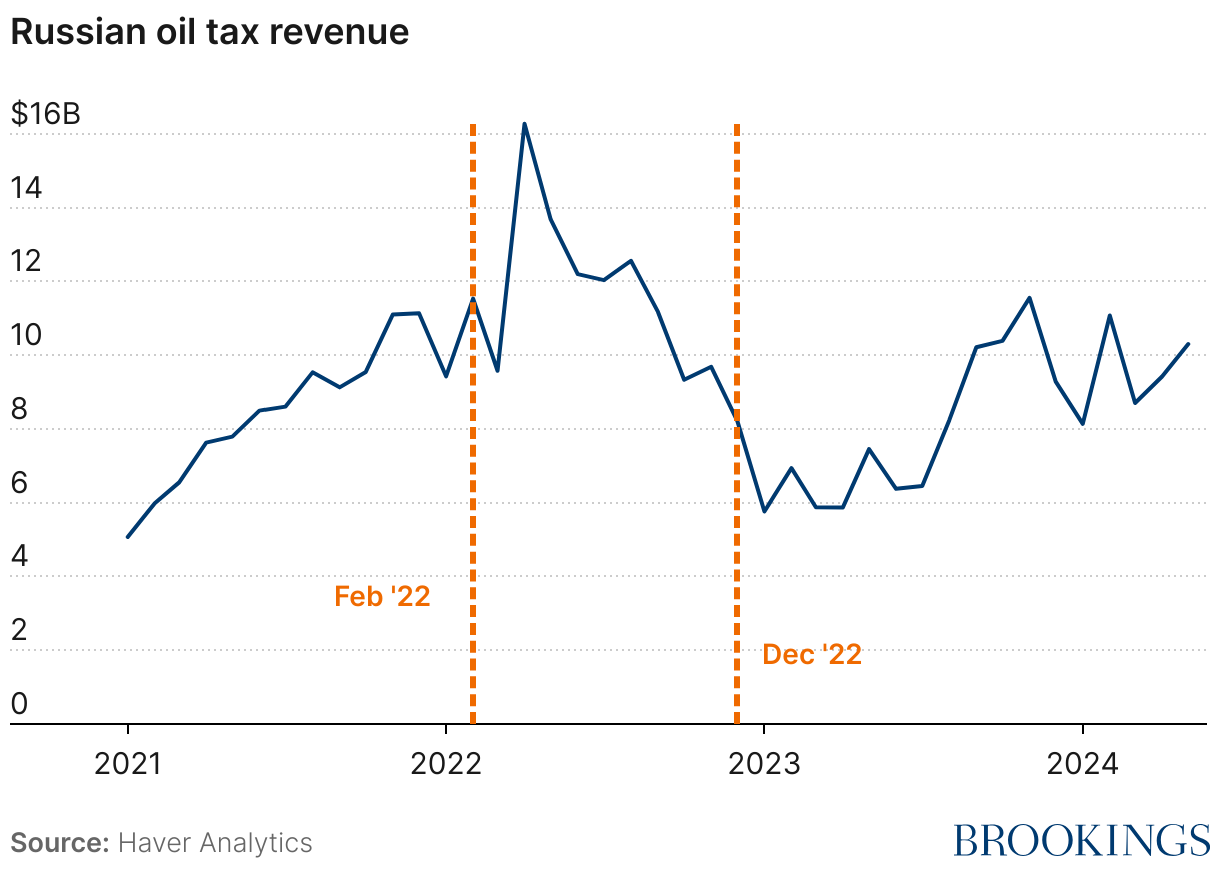

With export volumes stable, Russia’s oil tax revenues—critical to fund its war in Ukraine—have fluctuated with the price of Urals (Figure 2). In the months before and after the pre-announced implementation of the price cap in December 2022, Russian revenues remained depressed. According to the U.S. Treasury Department, Russian oil tax revenues fell by 40% over the first nine months of 2023 compared to one year earlier, while analysis from the Atlantic Council put the monthly revenue loss at around $5 billion through the first ten months of the cap. However, as the price of Urals has risen over the past year, so have Russia’s tax revenues on oil, a key challenge for the coalition of countries behind the price cap. Notable, too, is the closing of the Brent-Urals spread, suggesting that Russia has devised strategies for circumventing the price cap.

The closing of the Brent-Urals spread has been enabled by Russian countermeasures to circumvent the price cap, namely the cultivation of an expanded shadow fleet of aging tankers, often covered by inferior insurance provided by the Russian company Ingosstrakh. The expanded shadow fleet has allowed Russia to blunt the price impact of compliant service providers by shifting away from Western-provided services, which simultaneously reduces the leverage of non-Western trading partners like China. While the expanded shadow fleet ultimately means more oil revenue for Russia, the gain is somewhat offset by increased expenditures for obtaining the shadow fleet and higher trading costs—namely increased insurance fees. That being said, the key point is that limiting the scope of the shadow fleet is central to preserving the continued success of the price cap.

The case for sanctioning additional Sovcomflot tankers

The price cap achieved its goal of ensuring stable supply of Russian oil to the global economy, but the build-up of the shadow fleet has allowed Russia to export oil above the cap, boosting its economy and tax revenues. As a result, a second phase of the price cap was launched in October 2023, designed to enhance enforcement and increase the costs to Russia of using the shadow fleet. As part of this second phase, the U.S. rolled out a series of enforcement actions designating vessel owners, shipping companies, and an oil trader that were using western services to export Russian oil above the cap. On February 23 of this year, in an enforcement action coinciding with the two-year anniversary of Russia’s invasion of Ukraine, the U.S. also designated 14 tankers operated by Sovcomflot—Russia’s state-owned shipping company.

Despite these actions, Russia’s continued ability to trade around the cap has intensified calls for additional enforcement provisions. For example, Harvard scholar Craig Kennedy proposed making the Baltic a “shadow free” zone by requiring proof of adequate insurance, backed by a blocking threat (i.e., exclusion from the Baltic) for non-compliant tankers. Along similar lines, Simon Johnson and Catherine Wolfram proposed that a greater number of Sovcomflot tankers be subject to sanctions and that the sale of tankers to undisclosed buyers should be banned—arguing that such actions would increase the risk premia demanded by service providers that transact with Russia.

The most straightforward, and perhaps obvious, potential option facing U.S. policymakers is to expand on the February 23 action to designate 14 Sovcomflot tankers and sanction the remaining 100 Sovcomflot tankers that have yet to be identified for enforcement. Such a move would be consistent with prior actions and would meaningfully limit Russia’s ability to transact above the respective price caps. As we explain below, this incremental move would likely have limited, if any, impact on global oil prices.

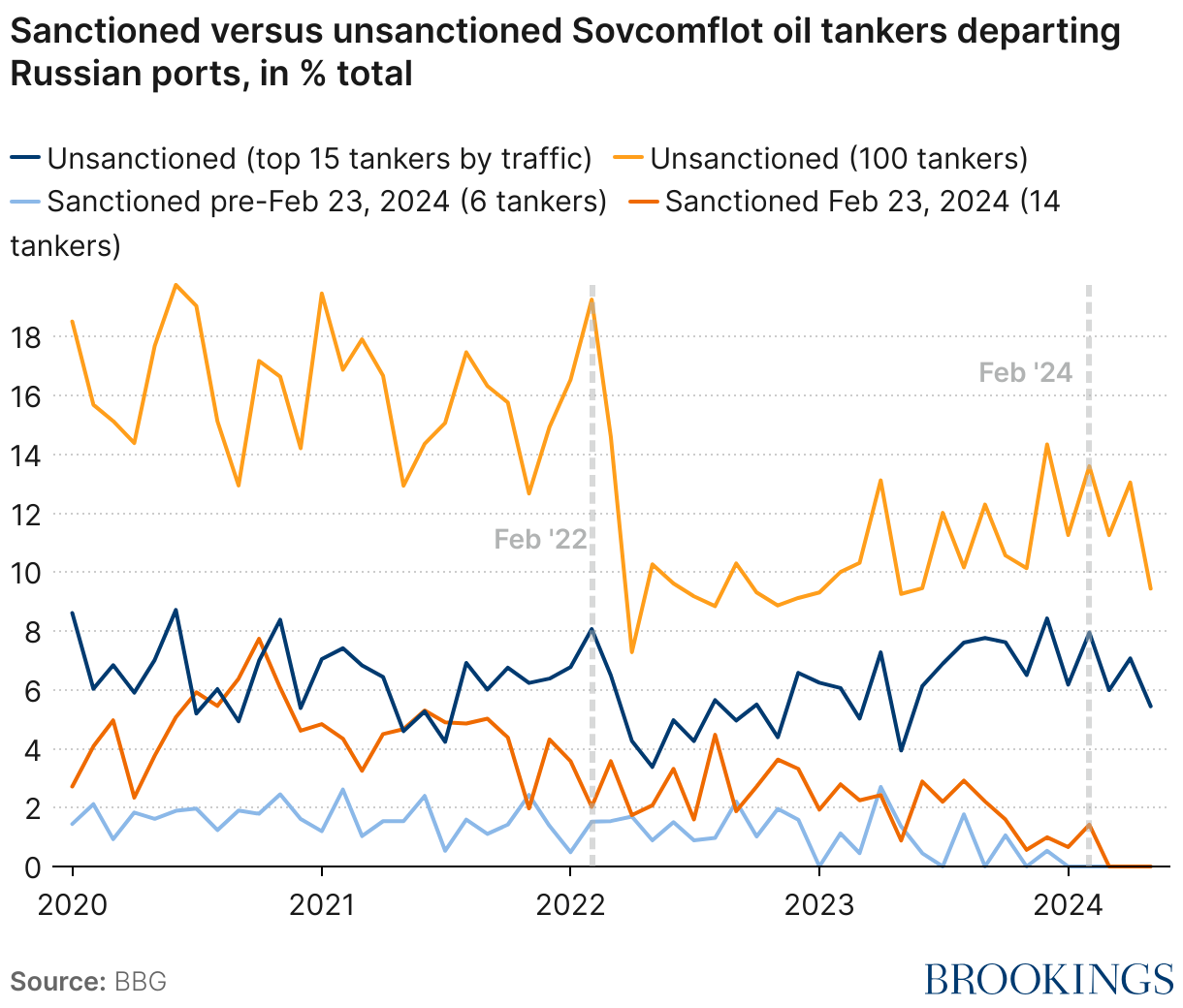

Sovcomflot currently has a fleet of 120 oil tankers according to its website. Twenty of these ships are now sanctioned, including the 14 ships sanctioned in the February 23 action and six oil tankers sanctioned prior to that. Bloomberg maintains a database called AHOY that tracks oil tanker traffic around the world. We use this database to track departures of all oil tankers departing Russian ports in recent years. These data cover around 85% of all oil tanker traffic out of Russia and are thus highly representative. We divide the Sovcomflot fleet into four groups: (i) the six ships sanctioned prior to February 23; (ii) the 14 ships sanctioned on February 23; (iii) the 100 ships that remain unsanctioned; and (iv) the 15 most active ships—measured by number of departures from Russian ports between February 2022 and June 2024—among the 100 unsanctioned Sovcomflot ships.

Figure 3 shows the importance of these four subsets of the Sovcomflot fleet in all of Russia’s seaborne exports of crude and refined product. The 100 unsanctioned Sovcomflot oil tankers currently account for around 10% of total seaborne exports out of Russian ports. Exports on Sovcomflot’s sanctioned oil tankers have fallen to zero, although it is possible that some continued activity is not captured in the Bloomberg data. Importantly, on average in 2023, the 14 now-sanctioned Sovcomflot ships accounted for 2% of total seaborne exports, but their designation on February 23 resulted in no oil price spike whatsoever, even as volumes on these 14 ships went to zero. As volumes on the 100 unsanctioned Sovcomflot oil tankers remained roughly stable around this action, it is likely that this volume was absorbed by Western-owned ships or the shadow fleet.

Within the fleet of 100 unsanctioned Sovcomflot oil tankers, activity is highly concentrated. We rank these 100 ships by their frequency of departure from Russian ports. The top 15 ships account for half of remaining Sovcomflot volume in terms of Russia’s seaborne exports. Table 1 in the Appendix provides details on these oil tankers, including the frequency of their departures from Russian ports, their size—most of these are Aframax oil tankers—and in what region they primarily operate. In principle, by designating these 15 ships, it is possible to target more than half of the remaining Sovcomflot export capacity out of Russia. To ensure little impact on price, the U.S. may want to calibrate future designations using this ranking to ensure that the overall volume effect is comparable to February 23. (On average in 2023, these 15 ships accounted for 7% of overall Russian seaborne oil exports versus 2% for the 14 ships designated on February 23.) That is, it may be worth sanctioning the remaining fleet of unsanctioned Sovcomflot ships in waves to minimize price effects.

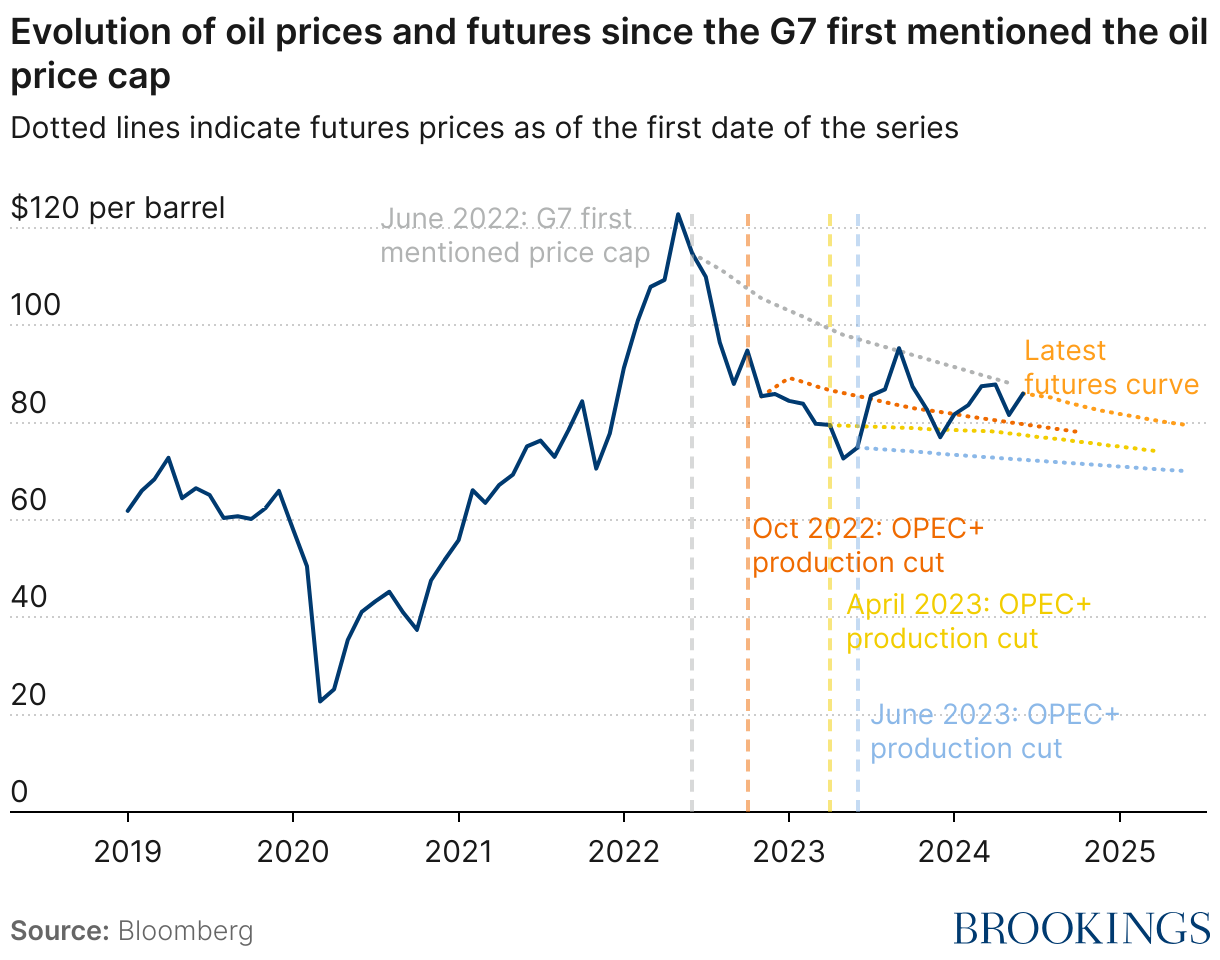

The big picture is that price effects arising from sanctioned Sovcomflot tankers are extremely unlikely. Figure 4 shows the Brent oil price along with oil price futures at the first mention of the oil price cap mid-2022 and subsequent OPEC+ production cuts. None of these instances appear to have had any material impact on oil prices. While this is far from causal, we think it validates the notion that further sanctions on the Sovcomflot fleet are unlikely to cause oil price spikes.

Conclusion

The designation of 14 Sovcomflot oil tankers earlier this year is an important precedent. It suggests that—for comparable volumes—there is no adverse impact on global oil prices. As a result, further such action on the remaining Sovcomfleet is highly desirable, since it will drive Russia’s seaborne oil exports to Western-owned or shadow fleet vessels, both of which should adversely impact the revenue Russia generates from these exports.

Given that activity among the unsanctioned fleet of 100 Sovcomflot ships is highly concentrated, we recommend sanctioning these ships in multiple rounds to keep volume effects on par with the February 23 action. With such a process in place, we anticipate little to no impact on global oil prices but suspect the action will meaningfully lower Russia’s revenue from the oil trade.

Related Content

2024

Authors

Appendix

Table 1 lists the top 15 unsanctioned Sovcomflot oil tankers by frequency of departure from late February 2022 when Russia invaded Ukraine through early June 2024. It lists the International Maritime Organization identification number (“IMO”) of each of these ships, the name of each ship, the type of oil tanker, and in what region these ships primarily operate. These 15 ships account for half of unsanctioned Sovcomflot volume out of Russian ports. The dark blue series in Figure 3 is made up of these 15 ships.

-

Acknowledgements and disclosures

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

Commentary

Why the US should sanction more Russian tankers

June 26, 2024