On the 40th anniversary of her accession to the British throne, Queen Elizabeth II remarked that “1992 is not a year on which I shall look back with undiluted pleasure. In the words of one of my more sympathetic correspondents, it has turned out to be an ‘Annus Horribilis.’” In the finance and economic development arena, 2022 may also be remembered as an Annus Horribilis. The year proffered an extremely difficult operating environment, marked by excess global volatility, severe geopolitical tensions, record-high inflation and tightening global financial conditions. Taken together, these headwinds significantly dented global growth prospects, derailing the incipient recovery from the COVID-19 pandemic downturn.

2022 was also the most damaging year in recent history for both stocks and bonds—the S&P 500 was down nearly 20%, its worst performance since 2008—and record-high inflation in both advanced and developing economies set the stage for one of the most aggressive, synchronized monetary tightening cycles in decades. At 8%, annual average inflation in the U.S. far overshot the Federal Reserve’s target levels, reaching heights not seen in 40 years. Steps taken by the Fed to try to bring price rises back toward its 2% target—including raising interest rates by 475 basis points in the space of a year—propelled the U.S. dollar index to a 20-year high. This had significant consequences for the developing world, including Africa, in terms of growth and fiscal and debt sustainability.

But the collapse of Silicon Valley Bank (SVB) and increasing stress in the U.S. financial system—which have raised the specter of a credit crunch and the likelihood of recession in the world’s largest economy, considering the magnitude of the tightening cycle and the shape of the yield curve—could lead the Fed to make a monetary policy pivot that strikes the right balance between its price-stability and growth-supporting objectives. Such a move would accelerate dollar depreciation and reduce the fiscal incidence of external debt servicing, which has exacerbated macroeconomic management challenges across Africa by dramatically raising the cost of imported goods and heightening liquidity constraints.

When policymakers in systemically important central banks began to adopt aggressive monetary tightening, most countries across Africa had to contend with growth-crushing and default-driven borrowing rates, in addition to major macroeconomic management challenges associated with capital flow volatility and sudden stops. Egypt was one case in point—global investors pulled out around $20 billion from local debt in the first half of 2022, putting tremendous pressure on the country’s exchange rate, which depreciated by more than 50% over the course of the year.

More than 60% of African countries’ currencies depreciated against the dollar in 2022, exacerbating inflationary pressures in a region where unemployment rates reminiscent of the Great Depression further complicate the challenges faced by monetary authorities. Earlier this year, the inherent tension of trying to curtail inflation without stymying growth manifested in South Africa. The Reserve Bank there was obliged to stick to its strict inflation-fighting position, pursuing successive interest rate hikes that risked curbing already anemic growth. South Africa’s economy will barely grow this year, with the International Monetary Fund estimating GDP expansion of 0.3%.

The combination of aggressive monetary tightening and the 12% appreciation of the dollar, which hit a two-decade high in September 2022, came at huge costs to Africa, especially for low-income countries with limited fiscal space. In addition to contending with higher costs of imported goods and default-driven borrowing rates, dollar appreciation handicapped policymakers’ ability to combat price rises. The exchange rate “pass-through” magnified already high inflation and further eroded African households’ purchasing power, raising the incidence of poverty after the sharp deterioration of living standards during the pandemic. But the rising incidence of poverty was further exacerbated by growth deceleration. A recent study by Maurice Obstfeld and Haonan Zhou found that 10% dollar appreciation leads to a decline in real GDP of around 1.5% relative to trend in emerging economies.

Aggressive monetary tightening has also constricted financial conditions and raised refinancing risks, especially in emerging market economies, most of which suffered landslide procyclical downgrades at the height of the COVID-19 crisis. The combination of tighter financial conditions and the sharp depreciation of local currencies increased the fiscal incidence of sovereign debt in countries that were already overburdened by default-driven borrowing rates. Africa incurred record amounts of debt service costs last year, forecast to total more than $72 billion, and those figures are projected to remain elevated in the coming years.

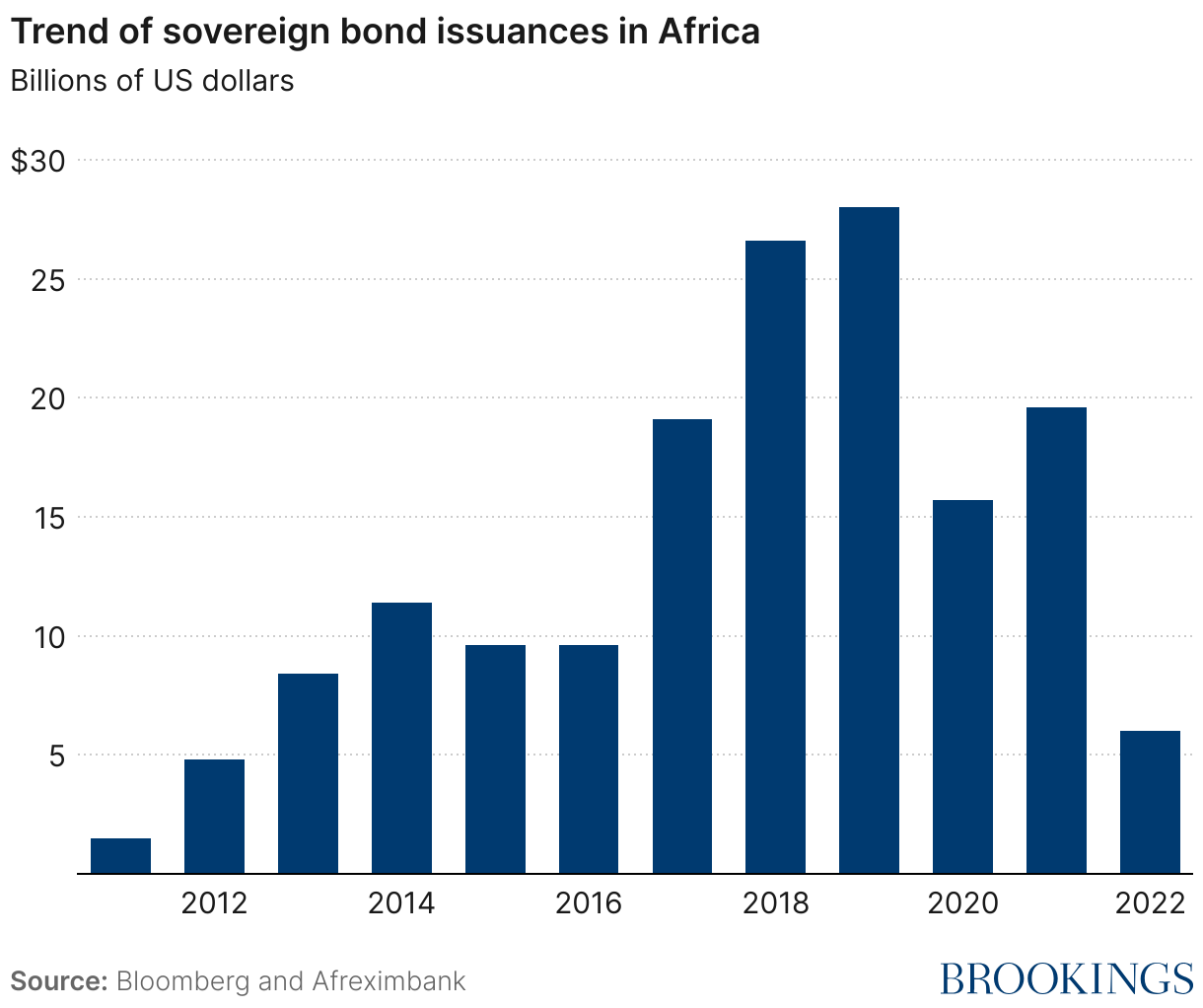

As more and more countries lost access to international capital markets, bond issuance collapsed. Only three African nations (Angola, Nigeria, and South Africa) successfully accessed capital markets in 2022, down from nine the year prior. Together, these three countries raised $6 billion, down from around $20 billion in 2021. And these three that could still access markets did so only under the yoke of higher exchange and interest rates.

Even more dramatic, however, was the impact of the retroactive bias of sharp dollar appreciation on Africa’s most vulnerable low-income countries. These economies received temporary relief under the G20’s Debt Service Suspension Initiative (DSSI), which deferred payments on external debt for a period of about 20 consecutive months ending in 2021 to enable governments to prioritize their pandemic response. Among the 32 African countries that are beneficiaries of the DSSI—45 countries globally received some temporary relief under the initiative—$11.2 billion of debt servicing due in 2020 and 2021 was suspended. But the sharp appreciation of the dollar against these countries’ currencies increased their debt burden in domestic currency terms by about $25 billion.

For Zambia, for instance, which moved from the DSSI to the G20’s Common Framework for Debt Treatments after defaulting on its debt, the depreciation of the kwacha (its local currency) raised its debt burden to $1.7 billion, more than double the $700 million of temporary relief available under the DSSI. Of the four African countries that have now applied to the G20 framework (Ethiopia, Chad, Ghana, and Zambia), all but Ghana were DSSI beneficiaries.

But following SVB’s collapse, which led the Fed to deliberate over fewer and smaller rate rises—perhaps even an outright pause as it contends with the new policy trilemma of price stability, growth, and financial stability—the operating environment in these vulnerable countries can be expected to become more favorable. Dollar depreciation, which began late last year as both volatility and the uncertainty around inflation abated, will continue, and perhaps even accelerate in the second half of this year as the downshift in U.S. market yields takes hold. The Fed’s return to a more incremental approach since the March meeting of its Federal Open Market Committee (FOMC)—when it raised rates by a quarter point versus the 0.75% increases that characterized late 2022—may demarcate a shift in monetary policy.

During its meeting held in May after the SVB demise, the Fed raised rates by another 25 basis points and signaled a potential pause, changing its forward guidance on the trajectory of interest rates. The Fed also took several measures in response, including creating the Bank Term Funding Program (BTFP) which provides lending to banks with collateral at par, providing liquidity in larger quantity through its discount window. Following the 25 basis point hike in July, it held interest rates steady in its September meeting, in line with market expectations.

The market has already been pricing in a policy pivot, with the Fed projected to begin cutting rates later this year. While Fed officials expect U.S. median interest rates will reach 5.6% by year’s end, in their most recent forecasts, they project that rates will fall to 5.1% by the end of 2024 and even further to 3.9% by the end of 2025. Since SVB’s demise, the dollar index has fallen to a one-year low, and the medium-term outlook suggests it is unlikely to return to the peak achieved in September 2022.

As the significant overvaluation of the dollar (based on the real effective exchange rate) is no longer supported by policy, the currency’s accelerated depreciation in light of the Fed’s monetary policy pivot will act as a fiscally neutral stimulus to both emerging market economies with access to international capital markets and low-income countries across the region. For most of these, and especially low-income countries that are largely “price-takers,” this will reduce the fiscal incidence of external debt servicing—as loans become less expensive measured in local currencies—as well as increase their fiscal space and alleviate pressure on their foreign exchange reserves.

It will also reduce the risk of more countries defaulting on their external debt, which will help to keep the region on an expansionary growth trajectory. World Bank research shows that debt restructuring is costly and leads to lower output growth in the short term. Moreover, the Fed’s policy pivot and dollar weakening could also increase risk appetite for African countries’ assets, helping to narrow ever-widening financing gaps. This may enable more sovereign and corporate entities to return to international capital markets and raise much-needed resources to drive investment growth after the collapse of bond issuance last year.

Of course, in our “polycrisis” world of great power rivalries, another geopolitical shock could always derail the normalization of global supply chains and stoke a new round of inflationary pressures, which might lead the Fed to go back to its laser-focused inflation-fighting mode. But in the immediate short term, by rebalancing the Fed’s policy objectives to account not just for price stability but also for growth and financial stability, the SVB debacle has perhaps accelerated the shift towards a global convergence of policy objectives between the Global North and South. The fiscal relief accruing to the latter as a result may well emerge as a break in the clouds for African countries amid the latest squall of U.S. financial turmoil.

But this global convergence of policy objectives is quite fortuitous, given that U.S. monetary policy is dictated solely by its own growth and financial stability objectives, even as decisions taken in Washington have implications for countries around the world. Hence, the more sustainable solution to Africa’s excessive exposure to global volatility is the diversification of sources of growth. This would boost intraregional trade, which history has shown to be an efficient absorber of adverse shocks, and yet remains dismally low in Africa. It hinges, too, on the development of domestic bond markets to promote local currency debt financing by way of hedging against the costly “original sin,” namely that African nations are largely unable to borrow abroad in their own currencies. Otherwise, countries across the region will always be just a few short steps away from another Annus Horribilis.

Author

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Silver lining for African countries of Silicon Valley Bank’s demise

October 5, 2023