Executive summary

The U.S. Postal Service traces its roots to the establishment by Congress of the Post Office Department in 1792, expanding a system first created in 1775 by Benjamin Franklin and the Second Continental Congress. Its purpose was to provide a fundamental public service: binding the nation through communication—similar to how roads physically connect the country. For much of U.S. history, the Postal Office Department operated as a government agency, funded by a combination of postage and service fees and congressional appropriations. However, financial and operational challenges led Congress to restructure it in 1970 into the United States Postal Service (USPS)—an independent agency within the executive branch, with the intention of improving efficiency.1 Despite these reforms, USPS continues to struggle with long-term financial challenges, fueling debates about the Federal government’s role in provision of postal services. President Trump and others have suggested that privatization can resolve these struggles. Some, however, argue that the postal services should remain a public function.

This report discusses implications of increased private sector involvement in the delivery of postal services in the U.S.

First, we highlight how market forces and the postal service’s obligation to provide quality nationwide mail service at uniform rates contribute to the financial challenges faced by the postal service.

Second, we highlight key differences between various ownership structures for reorganizing the postal service.

Third, we examine how European nations have approached postal reform and what adaptation of such a model to the US postal context might entail. Europe provides a compelling benchmark, having undergone a transformative shift when the European Union mandated competition in the postal sector starting in the late 1990s. We show that while privatization is linked to higher profitability, that it does not consistently improve service performance and is associated with higher prices. Moreover, financial and operational challenges persist across all ownership models, underscoring that privatization is not a universal solution to postal sector difficulties.

Finally, we consider lessons for potential reforms to the USPS. We conclude that policymakers should move beyond debates about ownership and instead focus on reassessing USPS’s mandate to ensure its funding model adequately supports its critical public obligations.

USPS: Structure, business model, mandates

The modern United States Postal Service (USPS) was established by the Postal Reorganization Act (PRA) of 1970, which transformed the postal service from a cabinet-level agency to a self-funded, independent establishment in the executive branch. This restructuring granted USPS greater autonomy by removing day-to-day operations from congressional control while maintaining federal oversight by a postal regulator to ensure service quality. Since then, USPS has primarily funded its operations through the sale of mail products and services. While the PRA reshaped its organizational structure, it preserved USPS’s public service mandate.

In fact, despite decades of reform, the core mission of the U.S. postal service has remained unchanged:

The Postal Service shall have as its basic function the obligation to provide postal services to bind the Nation together through the personal, educational, literary, and business correspondence of the people. It shall provide prompt, reliable, and efficient services to patrons in all areas and shall render postal services to all communities. (39 U.S. Code, Section 101)

This mission embodies the spirit of its Universal Service Obligation (USO), which requires that the postal service provide quality mail service to all Americans at a uniform rate, regardless of where they live. Early on, Congress recognized that the cost of maintaining the USO might stifle the postal service. If private companies were allowed to cherry-pick profitable urban areas, the government provider would be left to service costly rural areas. Thus, Congress conferred the postal service monopoly rights over the delivery of letter-mail (in 1845) and delivery of mail to private mailboxes (in 1934). However, because of market trends, the universal delivery mandate, and the diminishing monopoly value of its franchise, USPS is struggling to maintain financial viability.

Decline and disruption: Market trends in the postal sector

The USPS is one of the nation’s largest enterprises. It employs more than 600,000 people and had annual revenues of $78.2 billion in 2024 (similar to the operating revenue of Procter & Gamble). It manages more than 31,000 retail post offices (six times as many outlets as Walmart). It handles 44% of all the world’s mail. And, it has been operating at a loss since 2007, largely driven by declining mail volume and shift towards digital communication, sometimes referred to as electronic diversion.

First-class mail, marketing mail, and periodicals—which together account for more than half of the USPS revenue—have seen significant declines over the past 15 years (see Figure 1). First-class mail, a product over which USPS has exclusive delivery rights, has declined by 50%, from 91.7 billion pieces in 2008 to 46.2 billion pieces in 2023. Periodicals have fared even worse, with volume shrinking so much that the cost of processing and delivering them far exceeds the revenue that they generate for the USPS.

Declining letter delivery not only reduces direct revenue but also makes each delivery less profitable. This challenge is further exacerbated by the postal service’s USO in the context of an increasing number of delivery points—on average, 1.16 million new delivery points have been added every year since 2008. As USPS is required to expand its delivery network to accommodate the growing population, it must serve more addresses while handling fewer pieces of mail—placing an even greater strain on its financial sustainability. In 2023, for example, the Postal Regulatory Commission (PRC) estimated that the cost of USO exceeded the value of its monopoly rights by $2.6 billion.2

USPS also faces significant financial burdens tied to its status as a government-owned entity. For example, Congress, and not USPS, dictates the parameters of its retirement and workers’ compensation programs3, and this expense played a major role in driving the agency into deficit since 2006. Additionally, USPS is restricted in its ability to expand beyond the traditional mail services. Specifically, the 2006 Postal Accountability and Enhancement Act (PAEA) prevents USPS from offering new non-postal services, such as basic banking or other financial services, without congressional approval. Finally, USPS can only borrow from the U.S. Treasury, rather than raising capital through traditional capital markets. While this borrowing channel provides access to low-interest loans, USPS borrowing is subject to strict annual and total caps that have been unchanged for the last 30 years. USPS hit its maximum borrowing authority of $15 billion in 2012; by comparison, FedEx reported $35 billion in debt in 2024. These legislative restrictions imply that USPS is limited in its ability to reallocate revenue, diversify its service offerings, and undertake substantial capital investments that may be required for major reforms.

Corporatization, privatization, and liberalization: Options for postal reform

The terms corporatization, privatization, and liberalization are often used interchangeably in discussions about postal reform, but they represent three distinct approaches to re-organization, each with different implications.

Corporatization restructures a public entity to function more like a private business, granting it greater financial and managerial autonomy. This often includes the ability to set prices, streamline operations, and compete more efficiently in the marketplace. Privatization, by contrast, involves transferring a government-owned entity to private ownership, either fully or partially. Liberalization refers to the introduction of competition to a market that was previously closed to private firms. Unlike privatization, which transfers ownership, liberalization allows private companies to enter and compete alongside a government-run entity without requiring the transfer of ownership.

Corporatization of the postal service by PRA has not resolved the long-term financial challenges faced by the USPS. Meanwhile, the postal market has undergone significant liberalization through the innovation of work-sharing, which allows mailers to presort, transport, and handle mail before entering it into the US postal system at discounted rates. This has fostered greater competition in the mailing industry while leveraging the economic efficiencies of a single provider to fulfill the USO and provide last-mile delivery. USPS also already faces considerable competition from private companies, such as Amazon, FedEx, and UPS, in delivery of its competitive—and profitable—products, such as parcels.4

In the U.S. postal sector, further liberalization would require the relaxation of the postal monopoly over certain product segments and allowing private carriers to compete. Proponents of postal liberalization suggest that competition can drive innovation, improve delivery speed, and reduce costs through competition. Critics argue that liberalization can erode the financial stability of public services by allowing private competitors to operate in the most profitable markets, leaving the government-run entity with costly public service obligations but fewer resources to sustain them.

European postal reforms: A comparative perspective

The European Union’s (EU) approach to creating a single, competitive postal market among member states in the early 1990s offers a valuable comparative perspective on market liberalization. Liberalization was achieved through three EU Postal Directives over two decades. These directives, implemented between 1997 and 2012, required member states to gradually reduce the scope of national monopolies and open delivery segments to competition. While liberalizing the market, the EU also requires that member states ensure that a standardized Universal Service Obligation (USO) is maintained—either by one or several Universal Service Providers (USPs)—and provides guidance for appropriate compensation for associated costs.

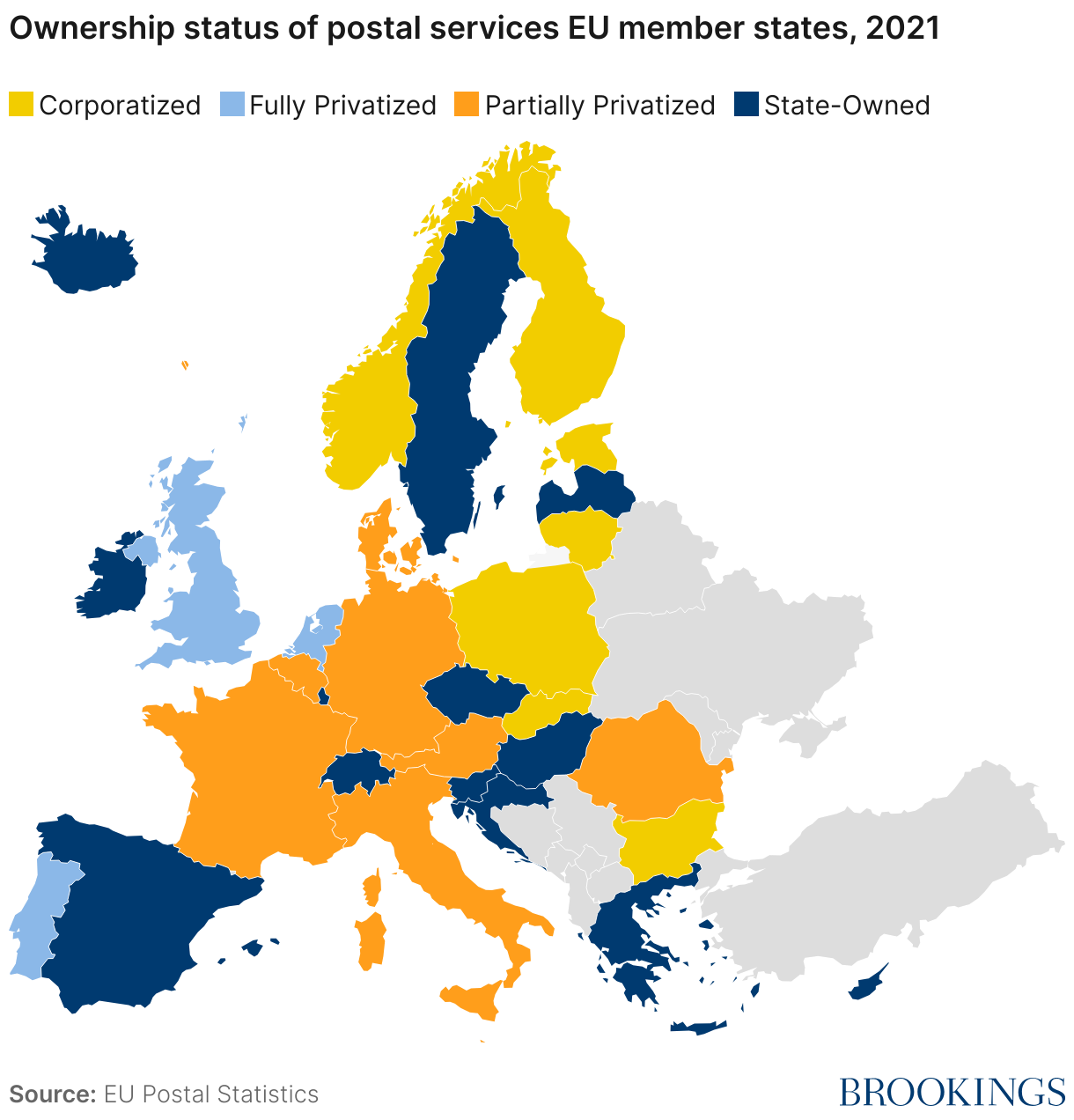

Importantly, these EU directives required liberalization of postal markets rather than privatizing national postal operators. As a result, the current ownership of postal operators varies across member states. Some countries have fully or partially privatized their national postal operators, whereas others maintain state ownership with a reduced scope of service.5 Figure 2. shows the ownership status of the postal operator designated as the USP.6 Three EU member states are fully privatized (Netherlands, Portugal, and the United Kingdom7), meaning the state has no ownership. Eight EU member states were partially privatized, which we define as those in which the state has an ownership stake less than 100%. Eight member states were corporatized, which we define as those legally corporatized with 100% state ownership. Finally, 13 postal operators were state-operated, which we categorize as those organized as a state-owned enterprise or those without categorization by the EU.

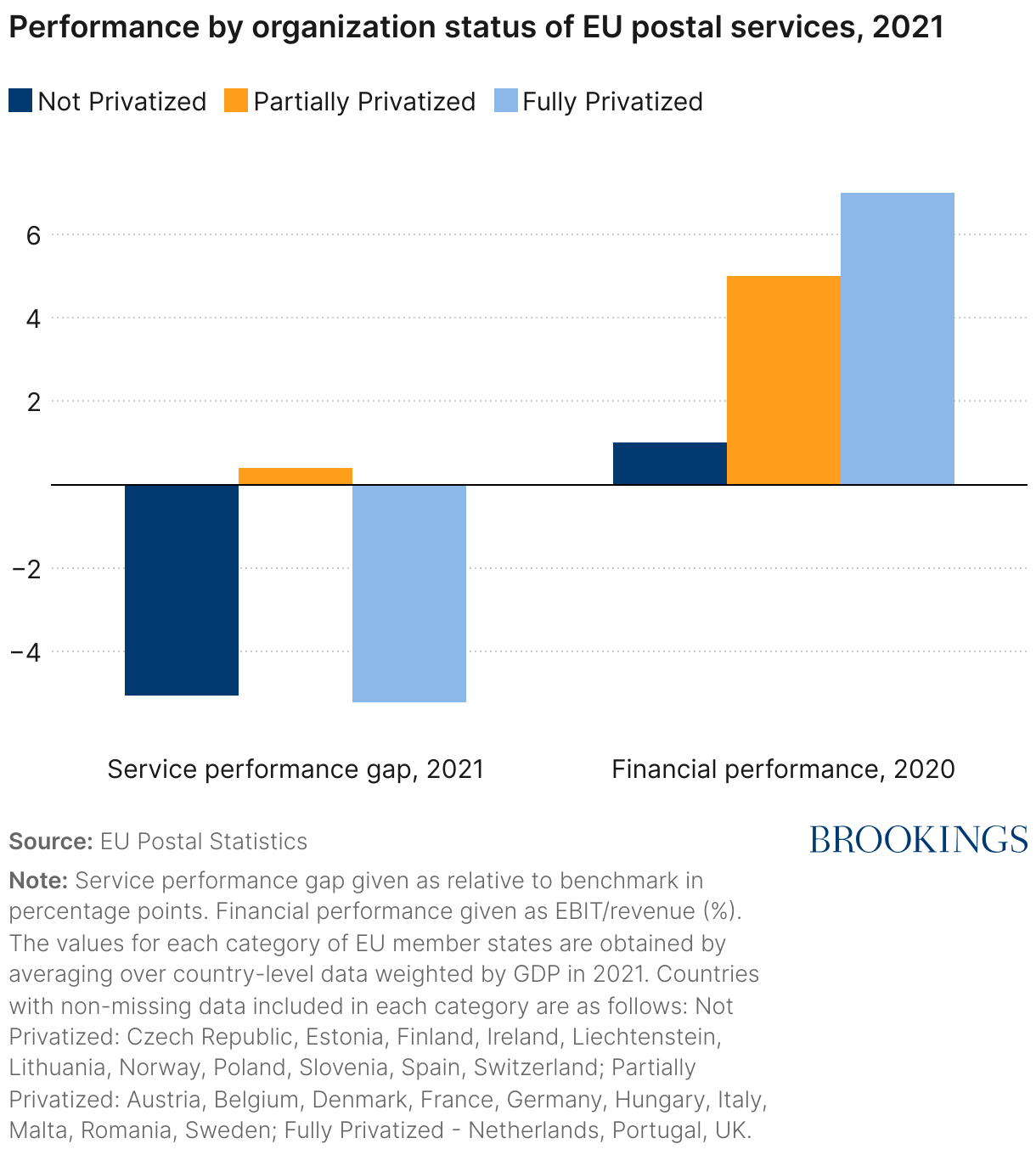

Calls for privatization of postal operators are typically made in response to poor service performance or poor financial performance, however evidence from Europe suggests that privatization is not a silver bullet. The left side of Figure 3 shows that both fully privatized and public USPs fall short of meeting their benchmark performance standards, and in similar ways. At the same time, privatization appears to be associated with improved financial performance: fully privatized providers have the highest margins and publicly owned providers have the worst margins (Figure 3, right side).

However, improved financial performance has come alongside rising prices. Figure 4 shows that from 2012 to 2021, partially privatized providers oversaw the fastest appreciation in the price of domestic letters. By comparison, prices of fully privatized and public operators followed similar trends. These patterns, however, are shaped by more than just ownership; differences in market demand across countries likely play a significant role.

Taken together, these trends highlight key insights about privatization:

- Privatization is associated with higher profitability.

- Full privatization, or a complete divestment of public ownership, is not associated with improved service.

- Partial privatization, or the introduction of private interest in a corporatized postal service, is associated with improved profitability relative to publicly owned USPs and improved service.

At the same time, these differences may not be caused by privatization. Each EU member state decided whether to privatize its postal operator as privatization was not mandated by EU directives. As of 2021, fewer than half of EU member states have either fully or partially privatized their postal operator. Those member states that chose to privatize were likely to be those that stood to benefit the most. This makes it difficult to determine whether these differences are a result of privatization or other differences among member states.

Finally, it is worth noting that in recent years several European postal operators have faced significant financial challenges. For example, PostNL, the fully privatized postal operator in the Netherlands, declared its current business model “no longer sustainable” due to declining mail volumes, increased competition, and increased costs for delivering parcels. Correos, Spain’s state-owned postal operator, has been grappling with significant financial and operational challenges, including declining mail volumes and employment, and historical losses. The Spanish government has responded by expanding the responsibilities of the USO to require the provision of basic financial services. Finally, PostNord, the corporatized postal operator of Denmark, recently announced that it will end all letter delivery due to declining letter volumes. These examples highlight that postal market challenges persist across different ownership structures and in spite of privatization.

USPS is a poor candidate for privatization

With lessons from European reform in mind, USPS is likely to be a poor candidate for privatization.

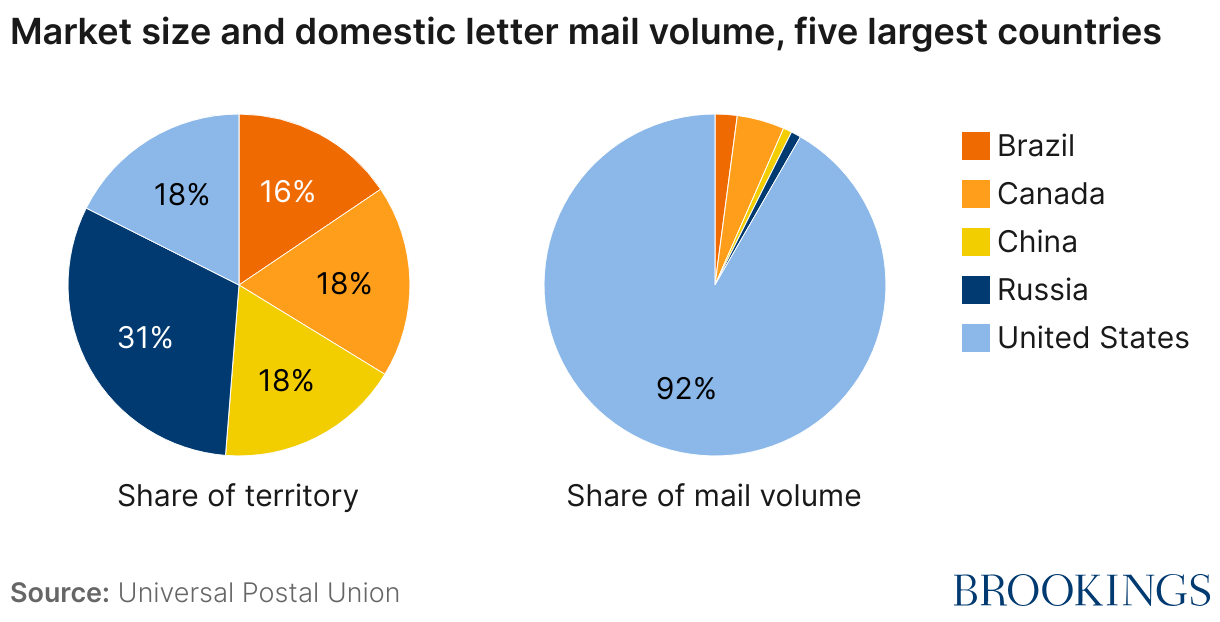

To begin, the scope of the U.S. postal market requires an operational scale unlike any other national operator around the world. USPS services 154 million residential delivery points and 12.6 million business delivery points over an area of 9,689,091 km2, or more than 17 times the size of the largest EU member state, France (551,500 km2). More broadly, the five largest postal markets based on geographic area are, in order: Russia, Canada, the United States, China, and Brazil. While Russia is the largest by land area, the other four countries are comparable in size (Figure 5a). However, USPS alone handles 92% of the total domestic letter volume across these markets (Figure 5b), highlighting its outsized role in global mail delivery. These geographic factors impose substantial cost pressures on the U.S. postal system that are unlike in any other market.

USPS must also contend with a broader public service obligation than many other operators, both in Europe and beyond. For example, it is required to provide a range of postal products and maintain six-day-per-week mail and parcel delivery—obligations that exceed those of many international counterparts. By comparison, other global UPSs enjoy fewer mandated delivery days, more flexible delivery times, and varying service between urban and rural areas or between letter and parcel mail.

Recognizing that universal service would not be naturally provided by a privatized postal operator, many governments have established standards for financial compensation for the designated USP. USPS, by comparison, receives just 0.1% of its total revenue from Congressional appropriations.8 Instead, the value of USPS’s mail monopoly is intended to compensate for the costs of servicing USO, but the value of the postal monopoly has not been adequately compensated for the costs of servicing its USO in a majority of the last 15 years. Given that the USO represents the core public service mission of USPS, any attempts at privatization must directly confront the preservation—and financing—of the USO.

USPS’s public service expands beyond the provision of mail services. USPS provides support for agencies in response to crises as an integral part of the National Response Framework. For example, USPS assists with the transportation and distribution of medicine in the event of a national disaster or emergency and letter carriers identify vulnerable persons in need of care or assistance. USPS has also implemented tight security precautions including the installation of biohazard detection systems to detect bomb and anthrax threats in the mail system. Finally, postal service workers were designated as essential workers during the COVID-19 pandemic, ensuring the continued delivery of letters and parcels while facilitating the nation’s largest vote-by-mail operation amid economic shutdowns and unprecedented disruptions. These responsibilities add to the public service cost of USPS.

Given USPS’s broad public service obligations, strong regulatory oversight is essential to ensure its continued accessibility and reliability. In fact, regulatory bodies around the world play a key role in ensuring that postal services remain accessible at affordable rates and acting as a safeguard against market distortions like anticompetitive behavior that might undermine fair access to postal services. Importantly, regulatory oversight exists regardless of whether a postal operator is state-owned, partially privatized, or fully privatized. In the U.S., this responsibility falls to the Postal Regulatory Commission (PRC), an independent federal agency established by the PRA of 1970 to oversee USPS operations and service standards.

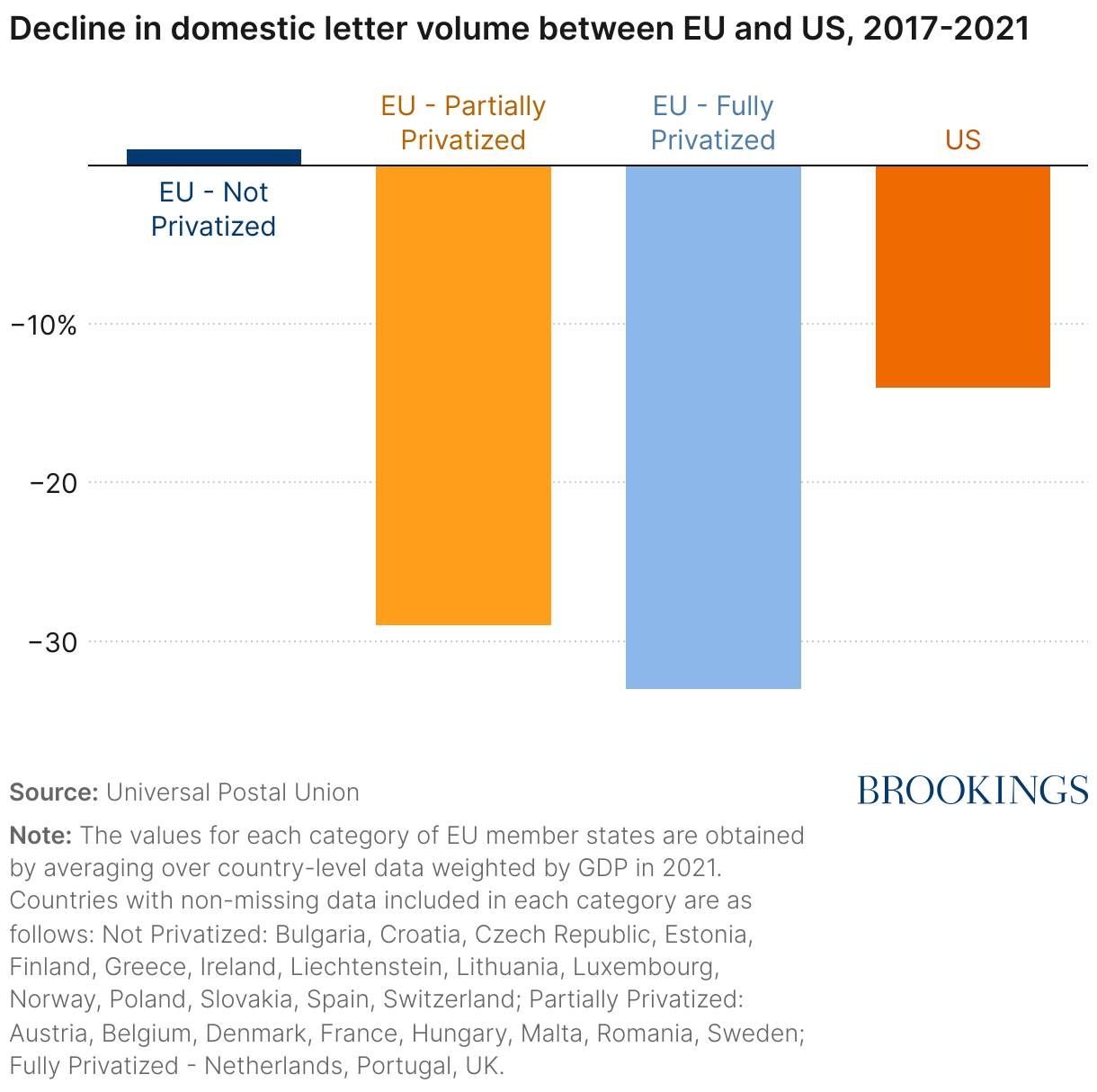

Finally, we note that postal operators across the globe are grappling with declining mail volumes and increased parcel delivery competition, challenging traditional business models. For example, EU member states with partially or fully privatized postal services have suffered steeper declines in domestic letter mail volumes than the U.S. (Figure 6). Some postal operators have responded by diversifying their revenue streams, offering, for example, basic financial services or extracting additional value from its real estate. National posts in Korea, China, Italy, India, Japan, and Taiwan earn most of their revenue from non-postal services, and China Post Group and Japan Post Group own two of the 25 largest banks in the world. USPS, however, is restricted in its ability to expanding its operations beyond the traditional postal services without legislative approval.

Conclusion

Policymakers must navigate a careful balance between ensuring the financial sustainability of USPS and preserving its vital public service role. The demands on USPS are substantial—it handles 44% of the world’s letter mail, operates a nationwide network of more than 31,000 post offices, and employs more than 600,000 people. Yet, as communication and e-commerce continue to evolve, USPS—like all postal operators—must modernize to remain viable. However, privatization is not the solution. Abandoning USPS’s public mission in favor of a purely commercial model would weaken the very foundation of universal mail service. The experiences of postal operators across the globe underscore that market-driven solutions alone do not guarantee affordable, reliable, or equitable service. Instead, privatization can lead to reduced service quality and higher costs for consumers without avoiding the financial struggles that face USPS today.

Reform should focus on modernizing operations, such as allowing USPS to expand into basic banking and other services that complement its core mission—while reinforcing its essential role in universal mail service, connectivity, and access to essential goods. USPS’s mandate “to bind the Nation together through the personal, educational, literary, and business correspondence of the people” remains just as critical today as when the Postal Service Department was first established in 1792. Upholding this mission requires a sustainable funding model that recognizes and supports its public service obligations, rather than one that forces it to compete on purely commercial terms. It also requires reaffirming the authority of the PRC to ensure accountability, maintain fair pricing, and uphold USPS’s public service commitment. A thoughtful approach—one that balances fiscal responsibility with the broader social value of universal postal access—is essential to ensuring that USPS continues to fulfill its public service mission for generations to come.

Related Content

Authors

-

Footnotes

- Subsequent legislative reforms, including the Postal Accountability and Enhancement Act of 2006 and the Postal Service Reform Act of 2022, introduced new financial and regulatory frameworks but left the fundamental structure of the Postal Service intact.

- The Postal Regulatory Commission reports both total cost of the USO and the value of the postal monopoly in its Annual Report to Congress in Tables IV-1 and IV-6, respectively. The valuation of the postal monopoly reflects an estimate how much extra revenue USPS earns because it has exclusive rights to deliver certain types of mail.

- The 2006 law required USPS to pre-fund its retiree health costs for the next 75 years. This required a contribution of more than $56 billion over ten years. USPS has not contributed to the retiree health fund since 2010. In 2022, the pre-funding mandate was repealed by the Postal Service Reform Act.

- In fact, there is a mutual interdependence between private delivery companies. The USPS provides last-mile deliveries for private companies, and they provide USPS with means for transporting mail via air.

- Some liberalization and privatization efforts predate the EU’s postal directives, reflecting broader national policy choices.

- The privatization status of postal operator in each member state is based on information reported by the European Union’s “Main Developments in the Postal Sector (2017-2021), Volume 2.” While these data reflect 2021 ownership, no subsequent ownership changes have occurred.

- While the United Kingdom is no longer a member state of the EU, its inclusion here reflects its status during the period in which privatization occurred.

- These funds cover the cost of free postage for the blind or overseas voting.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).