Author’s Note: I delivered these remarks at the Rethinking Macroeconomic Policy IV Conference held by the Peterson Institute for International Economics on October 12-13, 2017. I respond to a paper by Andy Haldane on rethinking financial stability and policies to achieve it. I focus on linkages from financial stability to macroeconomic performance, and new governance structures created for macroprudential policies. Measuring systemic risks and evaluating policies to reduce risks are relevant in the current environment given increases in asset prices and rising global credit.

Andy Haldane’s paper is a comprehensive review of current research on financial stability policy issues, and raises some important areas for future work to promote financial stability.[1] I will expand on two research areas related to implementing macroprudential policies. The first area is empirical estimates of the effects of financial conditions on economic growth and specifically on downside risks to growth. This work importantly translates financial stability risks into risks to output growth, and thus allows policymakers to use a common language for macroprudential policies and monetary policy or other macro policies. The second area is the governance structure for macroprudential policies, which is critical for actually taking actions. In particular, can monetary policymakers assume there are effective macroprudential authorities in place to implement policies to promote financial stability? Can monetary policymakers safely ignore financial stability considerations in their own policy deliberations?

For this discussion, I will define macroprudential policies as financial regulatory policies with time-varying parameters. There are important arguments for wanting to use dynamic policies in addition to structural time-invariant policies. In particular, risk-taking behavior is pro-cyclical, many regulations and models are pro-cyclical as well, and static regulations can be arbitraged, especially in countries with sophisticated nonbank sectors. These three reasons are not just abstract concepts, and they suggest important limitations to static structural policies on their own to promote financial stability.

In addition, the objectives for macroprudential policy can be broad. Andy points out that the Bank of England, as early as in 2009, raised the questions of whether it should target only the resilience of financial firms and markets, or whether it should also aim more boldly for smoothing credit cycles of households and businesses. In my view, there are strong economic arguments for macroprudential policies to aim for both, to target both lenders and borrowers, since there are negative externalities when either is stressed. Clearly, under-capitalized financial firms make economic growth highly vulnerable, and borrowers with high debt loads who are forced to deleverage can lead to a collapse in aggregate demand, and thus into a liquidity trap. But policies to reduce borrower’s debt burdens raise more political considerations than policies aimed at financial firms.

Estimating growth at risk from the financial sector

While there are strong arguments for wanting to implement macroprudential policies with dynamic parameters, there are challenges. A critical question is, when are risks sufficiently large to take pre-emptive actions? This question is more difficult to answer than responding to a crisis when it is obvious that there is a problem to be addressed. But such issues of timing are common to monetary policy as well, wherein central banks aim to raise rates before inflation gets too high, rather than wait and risk letting inflation expectations become unbounded. In this vein, there is recent, early-stage work to develop surveillance measures that express financial stability risks in terms of risks to future economic growth. I will mention three empirical exercises.

One exercise evaluates the effects of financial conditions on economic growth and whether they vary with macrofinancial imbalances, such as private nonfinancial credit. Excess private nonfinancial credit relative to its long-run trend has been found to predict recessions and crises, and now is reviewed regularly by many countries for setting the countercyclical capital buffer. For the US economy, we test the significance of excess credit for economic growth (Aikman, Lehnert, Liang, Modugno, 2017). In particular, we use a threshold VAR specification to test if the effects of financial conditions vary depending on whether the credit gap is high or low. In our model, financial conditions reflect risk premiums for asset prices and lending standards. We find looser financial conditions will boost GDP in near-term quarters in both low and high credit gap periods, but that growth is less sustainable in high credit gap periods than in low ones. That is, while the effects of financial conditions are positive in near-term quarters, they lead to negative growth in the medium term when the credit gap is high. These results suggest important nonlinearities, consistent with models of occasionally binding collateral constraints that can lead to sharp discontinuities. The results are robust to tests that high credit is not approximating for other factors, like a recession.

A second exercise is presented in the IMF October 2017 Global Financial Stability Report, Chapter 3. They present a measure of growth-at-risk from financial conditions, which provides a measure of financial stability expressed in terms of economic growth. They evaluate whether financial sector conditions can help predict the probability distribution of future GDP growth (building on Adrian, Boyarchenko, Giannone (2016) for the US). Using quantile regressions, they show the 5th, median, and 95th percentile of predicted year-ahead GDP growth based on financial conditions, estimated for 21 countries. They show tighter financial conditions have stronger effects on downside risks to growth relative to upside risks at one year-ahead. These results suggest looking only at median growth may ignore some key downside risks.

In particular, looser financial conditions predict lower downside risks in the near-term, roughly a horizon of one-year ahead. In contrast, higher borrower leverage (looser financial conditions) can signal greater downside risks in the medium term, at two-years to three-years ahead. That is, looser conditions reduce growth volatility in the near-term, but increase it in the medium-term, suggesting an inter-temporal tradeoff from looser financial conditions.

This growth-at-risk measure, which captures the expected path, volatility, and skewness of GDP growth, puts financial stability risks into the same language used for assessing other macro policies. Countries could track this growth-at-risk measure over different horizons over time. It has the potential to gauge the need for macroprudential policies at any time, and to evaluate the success of those policies.

A third empirical exercise reflects a combination of these two, and extends the growth-at-risk exercise by conditioning the growth effects of financial conditions on excess credit and testing for nonlinear dynamics. In preliminary work for eleven advanced economies, we find the combination of high credit and loose financial conditions—an exuberant period—leads to a greater increase in the volatility of growth in the medium term, indicating less sustainable growth and reinforcing the result of an inter-temporal tradeoff.

These three examples test and find results consistent with a framework that looks at financial stability as the ability of the system to absorb rather than amplify any negative shocks (see Adrian, Covitz, Liang, 2015). Vulnerabilities can build in a predictable way, and result in greater downside risks because of occasionally binding collateral constraints that lead to sharp discontinuous adjustments through aggregate demand externalities, fire sales, and investor runs.

Governance structures for macroprudential policies

An important part of effectively setting macroprudential policies is having appropriate governance structures in place for evaluating risks and taking policy actions. This issue is especially interesting in the current environment, as many advanced economies are concerned that inflation remains below target, while asset valuations are rising and becoming unsustainable. At the same time, global credit is rising, as reported by the IMF in its October 2017 Global Financial Stability Report. A current question is what entities are monitoring systemic risks that could arise from the combination of high asset prices and rising credit, and taking pre-emptive actions to prevent a possibly costly fallout if asset prices were to drop sharply?

In a paper with Rochelle Edge, we evaluate new macroprudential authorities to answer the question of who makes decisions about dynamic macroprudential policies. We constructed a new dataset of macroprudential authorities for a sample of 58 countries. Macroprudential policies likely require a good deal of coordination across regulators and a greater focus on time-varying risks or on non-regulated institutions, and thus may warrant new governance arrangements. The database is based on public official documents, reflects information through 2016, and we are making it available to others.

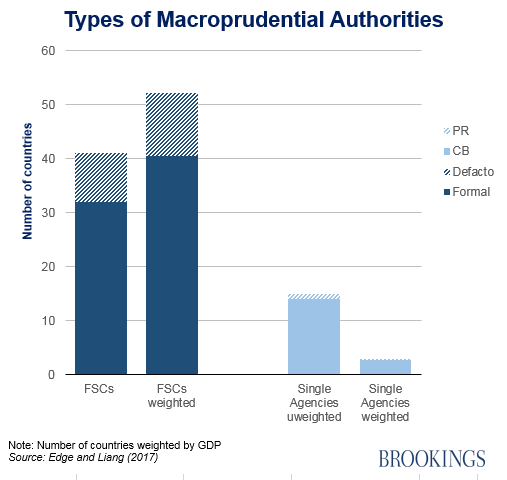

Many countries (41) have established inter-agency financial stability committees (FSCs), formal or de facto, and 15 countries have designated a single entity to be the macroprudential authority. The single entity is almost always the central bank, which for these countries is also a prudential regulator. Weighting the arrangements by GDP shows that larger countries set up FSCs, while smaller countries rely on the central bank to be the single authority (Figure 1). No country in our sample created a new independent agency with new powers, but instead built on microprudential regulatory structures already in place. It appears that since microprudential regulators were not set up to implement macroprudential policies, countries chose to establish committees by including the central bank and often the ministry of finance. In terms of what governs global activity, committees clearly are the arrangement to focus on.

To evaluate the committees, we first looked at membership and leadership. FSCs in the 41 countries typically have between three and five voting members. Membership is important because the different agencies have different skills and objectives, which will affect macroprudential policy choices. Many international bodies have recommended that central banks have a prominent role in macroprudential policies, because of their analytical expertise for time-varying risks and operational independence in the conduct of monetary policy. However, given that some macroprudential policies may involve distributional choices, finance ministries as representing elected officials may be needed to provide legitimacy to the FSCs, though they may be less willing than central bank to implement unpopular policies. Our data show that central banks are on all FSCs but one, and are the sole chair of the FSC in 12 countries. However, finance ministries are more likely to be the sole chair of the FSC than is the central bank: ministries of finance (or the government) claim the sole chair in 21 countries. Prudential regulators are always on the committees, but are never a sole chair, likely reflecting their focus on microprudential issues.

Judging the effectiveness of financial stability committees is somewhat subjective. But we can use three criteria that the IMF (2014) has set out as important: Can they coordinate, do they enable taking actions, and are they willing to act?

Coordination. All the FSCs state they work to promote information sharing. The FSCs appear to have the right set of members. We test the hypothesis that FSCs are set up to facilitate coordination against taking advantage of skills of the central banks, and find evidence of setups reflecting a greater need for coordination. In this way, FSCs are a step forward.

Ability to act. We looked at whether FSCs themselves had any specific tools, like the authority to direct actions of its members, countercyclical capital buffer, stress tests, or loan-to-value ratios. Only two FSCs—in the UK and France—have hard tools, which means they can direct an action of their members. Another nine have “comply or explain” powers, which means the FSC can publicly express a view that an agency should take an action, but the agency has a choice and can choose to explain why it does not. That indicates that most FSCs (30) meet just to share information.

Of course, the separate regulators often have the authority to set policies, and the central bank can provide the time-varying analysis to assess risks. But the regulators may not, on their own, have financial stability mandates, and so there may be a disconnect between the authority over tools and responsibility for financial stability.

Willingness to act. This criterion is the hardest to assess, and it is too early to draw conclusions since most of the FSCs were not established until after 2010. But most FSCs do not have tools and macroprudential actions might be unpopular (“taking away the punchbowl”); in the absence of clear mandates, it is hard to see how new committees will want to take forceful actions to deter financial stability risks from rising, especially if there is a cost to current growth. But willingness to act is an area to track over time as conditions warrant more actions.[2]

In the meantime, monetary policymakers should not assume that new committees will take actions to offset pro-cyclicality in the financial sector to reduce dynamic financial stability risks. While new FSCs are formal arrangements to meet regularly and exchange views on financial stability, the lack of tools and political independence will limit the ability of new FSCs to act.

Conclusion

There has been substantial progress to increase the resilience of the financial system since the financial crisis. Policymakers now should evaluate the net effects of the substantial set of new regulations on growth, although financial systems are still adjusting and it may yet be too soon to make major changes.

More work is needed to develop frameworks for implementing dynamic macroprudential policies, as there are potential large benefits from developing these policies. Macroprudential policies can be an important complement to monetary policy, and countries that use both have the potential to achieve greater macroeconomic stability than if they relied only on monetary policy. On the framework, I am optimistic on models that define a target based on risks to future economic growth, but am less optimistic that the new governance structures that have been set up are able and willing to take actions. For most large countries, monetary policy may be the only time-varying macro-stabilization tool, and monetary policymakers should be aware of the limitations of macroprudential policies.

[1] Andrew Haldane (2017). “Rethinking Financial Stability.” Speech at the “Rethinking Macroeconomic Policy IV Conference,” Peterson Institute for International Economics, Washington, DC, 12 October 2017.

[2] Lim, et al. (2013) look at whether a more important role for the central bank leads to more timely macroprudential policy actions, based on a sample of 31 countries through 2010. While they find evidence of somewhat more rapid responses, they do not distinguish whether the benefits might arise from less need to coordinate when the central bank is a single authority or if it has better skills for implementing time-varying policies.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Rethinking financial stability and macroprudential policy

December 4, 2017