The findings in this report were discussed at an event on March 19, 2024. You can watch the full event here.

Tax filing may well be America’s least favorite indoor sport. Each year, new forms and rules can overwhelm even seasoned tax experts.

It does not have to be this way. In a new paper and project, I propose and analyze several major revenue-neutral sets of federal income tax reforms, each of which would create a simpler and more progressive system. A new interactive tool on the Urban-Brookings Tax Policy Center website allows anyone to compare their filing requirements and tax burdens under the alternatives and the current system. A more detailed paper provides additional background and context.

There is massive potential for simplification. The tax code is riddled with special provisions that are difficult to interpret and enforce. It also requires taxpayers to collect information that the IRS already has, while allowing some forms of income to go untaxed or lightly taxed and imposing heavy burdens on others.

Together, those provisions place an enormous burden—in time, money, and mental energy—on honest taxpayers trying to legally minimize their tax liability. The provisions also create both incentives and opportunities for people to cheat.

The problem is that simplifying the tax system cannot occur in a vacuum. The tax system did not get complicated by accident. The provisions in the code were all inserted for some purpose, whether to promote fairness, economic growth, social policy goals, or better tax compliance. For example, numerous tax subsidies help people pay for college, get childcare, or buy a home.

As a consequence, any effort to simplify taxes will have collateral effects. Some reforms raise more revenue than others. Some could make the tax code more progressive, support social policy goals, or boost economic activity. But simplification efforts will inevitably involve trade-offs with other desirable policy goals.

Because taxes are deeply embedded in the nation’s economic, social, and institutional structures, systemic changes meant to simplify the income tax may give rise to new complexities. When the rules change, there needs to be a transition plan. The IRS has to come up with transition rules, new definitions, forms, and other new procedures. In short, tax simplification requires tolerance of “rough justice”—taxpayers who have taken advantage of the gaps in the current tax code may not like the new system’s outcomes.

The factors that generate complex tax systems—the existence of policy trade-offs, the complexity of families and businesses, the role of lobbyists, etc.—are not going to go away. Let’s take a simple example – suppose you want to subsidize childcare costs but not include money parents spend on ski lessons for kids in Aspen, Colorado. Treasury would need to write a rule that covers every situation in between and place each squarely on one side of the line or the other. Ski resorts would have to learn and understand that rule and try to get around it, perhaps offering childcare separate from other ski resort amenities.

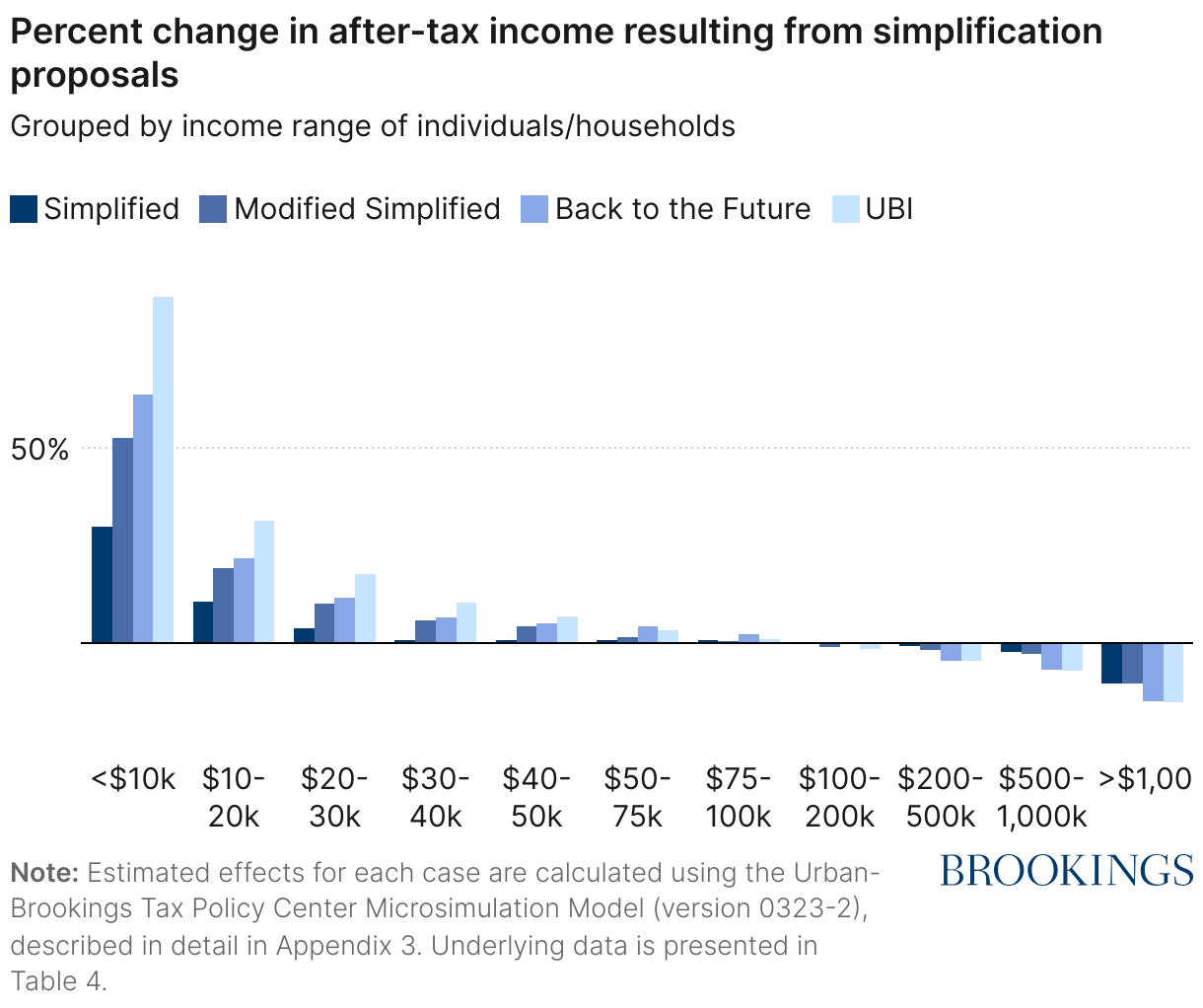

Against this backdrop, the first reform plan I describe would eliminate all itemized deductions, credits, and preferential tax rates in the system. Taxpayers would instead receive a new refundable personal credit of $1,000 cash for each family member. A new refundable work incentive credit would depend on an individual’s own earnings (without regard to family income) and could be administered by the Social Security Administration, without the need for 15 pages of rules overwhelming lower-income households trying to access the Earned Income Tax Credit.

An alternative plan could build on the first by enhancing its progressivity. Raising the standard deduction—$27,700 for married couples in 2023—to $100,000 ($50,000 for singles) and the new personal credit to $2,800 per person ($11,200 for a family of four) could be funded with a 10% value-added tax (VAT), a levy that exists in almost every other country in the world. This plan, based on work by tax professor Michael Graetz, would eliminate the need to file an income tax form for the vast majority of Americans.

Or, if we really wanted to help the poor, we could make all the changes in the first plan, create the VAT, and raise the personal credit to $3,900 ($15,600 for a family of four), effectively creating a Universal Basic Income (UBI) for all Americans.

Any of these systems would allow the Treasury to pre-populate tax forms for most taxpayers, as is done in many countries, eliminating a major source of hassle. And the IRS’s nascent direct-file system could be used for an even greater share of tax returns, saving taxpayers time and money.

Tax simplification is a long-standing issue that garners widespread support, at least in principle. And it’s technically feasible. But most existing taxes—and their reasons for inclusion in the tax code—are often far more complex than it seems on the surface. A concerted effort to simplify taxes will face an uphill battle. But simplification would make a lot of people a lot happier and is a credible way for policy makers to tangibly influence the lives of their constituents.

Author

-

Acknowledgements and disclosures

The author thanks Nora Cahill and Sam Thorpe for outstanding research assistance; Muskan Jha, Jessica Kelly, Gordon Mermin, Silke Taylor, and David Weiner for Tax Policy Center model calculations; Chye Ching Huang, Adam Looney, Elaine Maag, Eric Ohrn, Sarah Reber, and David Weiner for helpful comments and discussions; and California Community Foundation for generous funding.

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).