This paper is part of the Spring 2025 edition of the Brookings Papers on Economic Activity (BPEA), the leading conference series and journal in economics for timely, cutting-edge research about real-world policy issues. The summary below was drafted based on the paper’s conference draft presented at the Spring 2025 BPEA Conference on March 27-28, 2025. (Conference drafts, session recordings, and presentation slides are available via the link.) Submit a proposal to present at a future BPEA conference here.

*Final version posted: December 2025

Final paper with final comments, discussion summary, and appendix

Sun Belt cities such as Miami and Phoenix that once offered affordable housing are starting to resemble high-priced coastal markets like New York and Los Angeles, according to a paper discussed at the Brookings Papers on Economic Activity (BPEA) conference on March 28.

Until the 2000s, Sun Belt cities built housing at high rates and buyers were able to purchase homes at prices not greatly in excess of production costs (materials, labor, and land), according to the paper, “America’s Housing Affordability Crisis and the Decline of Housing Supply.” (*The paper’s title was updated in the final version to “America’s Housing Supply Problem: The Closing of the Suburban Frontier?“)

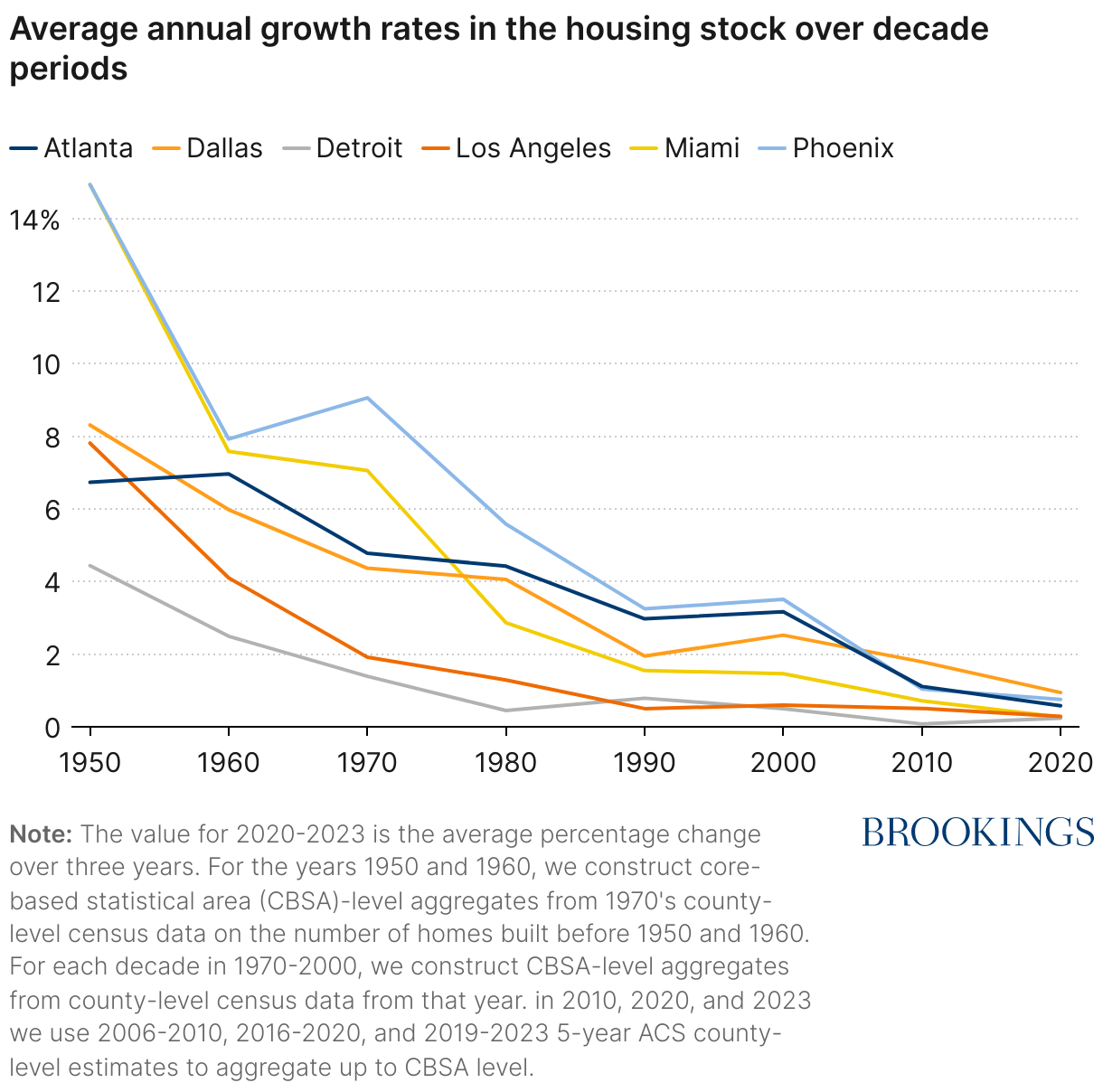

But, starting around 2000 and especially during the 2010s construction rates in the Sun Belt fell toward levels long-experienced by supply-constrained coastal markets as well as by Midwestern metropolitan areas grappling with low housing demand as the result of deindustrialization, according to the paper. Consequently, Sun Belt affordability declined.

The authors, Edward Glaeser of Harvard University and Joseph Gyourko of the University of Pennsylvania, used a model of housing supply and demand to analyze construction and price trends in Census Bureau data from 1950 to 2023. They focused in particular on Atlanta, Dallas, Detroit, Los Angeles, Miami, and Phoenix.

Nationally, the housing stock more than doubled from 36 million units in 1950 to more than 86 million in 1980, according to the paper. By 2023 it had reached 144 million units. But the annual growth rate slowed from 4% in the 1950s to 0.6% in the 2010s.

Through much of that period, housing construction in the Sun Belt far outpaced production in coastal areas. For instance, the stock of housing units in Phoenix grew at a 9.1% annual rate in the 1970s, 5.6% in the 1980s, and 3.3% in the 1990s. Meanwhile Los Angeles’ housing stock grew at a 1.9% rate in the 1970s, 1.3% rate in the 1980s, and 0.5% in the 1990s. By the 2010s, average annual growth rates had converged—to 1.0% for Phoenix and 0.5% for Los Angeles.

Meanwhile, housing prices adjusted for inflation and quality are at a historic high, more than 15% above the previous peak reached during the housing bubble that preceded the 2007-2009 financial crisis. Inflation-adjusted price increases generally were modest in Sun Belt markets until about 2000 but accelerated after that. For instance, Phoenix (where prices in early 2024 were running 2.5 times higher than their 1975 values) is catching up to Los Angeles (where early first quarter 2024 prices were four times their 1975 level).

The authors examine possible reasons for increased prices and conclude that decreased supply is responsible. Increased interest rates after the COVID-19 pandemic and increased production costs only partially explain today’s higher prices, particularly in the Sun Belt.

Gyourko, in an interview with the Brookings Institution, said the “coastal-ization” of Sun Belt housing markets endangers an important safety valve in the U.S. economy.

“It wasn’t so bad when the coasts became supply-constrained and incredibly expensive, because people could move to super-high-job-growth cities with affordable housing like Atlanta, Phoenix, Dallas, and Miami,” he said. “If this goes away, it will be the first time in American history where we don’t have affordable housing markets with high job growth.”

Authors

Authors

Discussants

CITATIONS

Glaeser, Edward, and Joseph Gyourko. 2025. “America’s Housing Supply Problem: The Closing of the Suburban Frontier?” Brookings Papers on Economic Activity, Spring: 375–425.

Baum-Snow, Nathaniel. 2025. “Comment on ‘America’s Housing Supply Problem: The Closing of the Suburban Frontier?’” Brookings Papers on Economic Activity, Spring: 426–440.

Molloy, Raven. 2025. “Comment on ‘America’s Housing Supply Problem: The Closing of the Suburban Frontier?’” Brookings Papers on Economic Activity, Spring: 441–450.

-

Acknowledgements and disclosures

Joseph Gyourko is an advisory board member of CenterSquare Investment Management, which invests in various housing sectors and markets. He gratefully acknowledges the financial support from the Zell/Lurie Real Estate Center at Wharton’s research sponsor program for this paper. Edward Glaeser is a lifetime trustee of the Urban Land Institute, and he receives compensation for occasional speaking engagements with real estate investment organizations.

The authors appreciate the comments of discussants, Nate Baum-Snow and Raven Molloy, as well as the editors, Janice Eberly and Jón Steinsson, and conference participants on earlier versions of the paper. They also benefited from the excellent research assistance of Manya Gauba, Flora Gu, Braydon Neiszner, and Lydia Qin. Naturally, the authors are responsible for all content.

Discussant Raven Molloy is a deputy associate director at the Federal Reserve Board. She would like to thank Andrew Paciorek and Daniel Ringo for helpful discussions and Allison Shertzer and Sarah Quincy for sharing their data. The results and opinions expressed in her comment reflect her views and should not be attributed to the Federal Reserve Board or the Federal Reserve System.

David Skidmore authored the summary for this paper. Chris Miller assisted with data visualization.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).