This week, House Ways and Means Committee Chairman Jason Smith (R-MO-08) and Senate Finance Committee Chairman Ron Wyden (D-OR) announced the framework for a bipartisan tax bill, including reforms to the Child Tax Credit (CTC) for the 2023 through 2025 tax years. While the proposed bill would have positive impacts for millions of low- and moderate-income families, future legislation will need to go much farther if it is to adequately support children living in deep poverty.

What is the Child Tax Credit?

The Child Tax Credit is a provision of the tax code that reduces tax liability up to $2,000 in credit per child. The CTC is partially “refundable,” meaning that low-income families can get up to $1,600 per child from the IRS even if they don’t owe any federal income taxes.

Though the CTC operates through the tax code, because of its refundability it is best seen as a key part of the safety net to support low-income families. Entitlement to cash assistance ended with the 1996 welfare reform, and the Temporary Assistance for Needy Families program that replaced it has eroded substantially in the past two decades. Tax programs like the CTC and the Earned Income Tax Credit are picking up much of the slack.

Not everyone is eligible for the CTC’s $1,600-$2,000 per child, however. The credit phases out for very high earners (starting at $200,000 for single parents or $400,000 for married parents). But the bigger source of controversy is at the lower end of the income distribution. In order to qualify for any CTC, families must show at least $2,500 dollars in earnings over the year, and the credit then phases in at a rate of 15% per dollar of earnings over $2,500. That means many low-income families only get a partial credit or no credit at all; more than a quarter of children do not qualify for the full credit because their parents don’t earn enough.

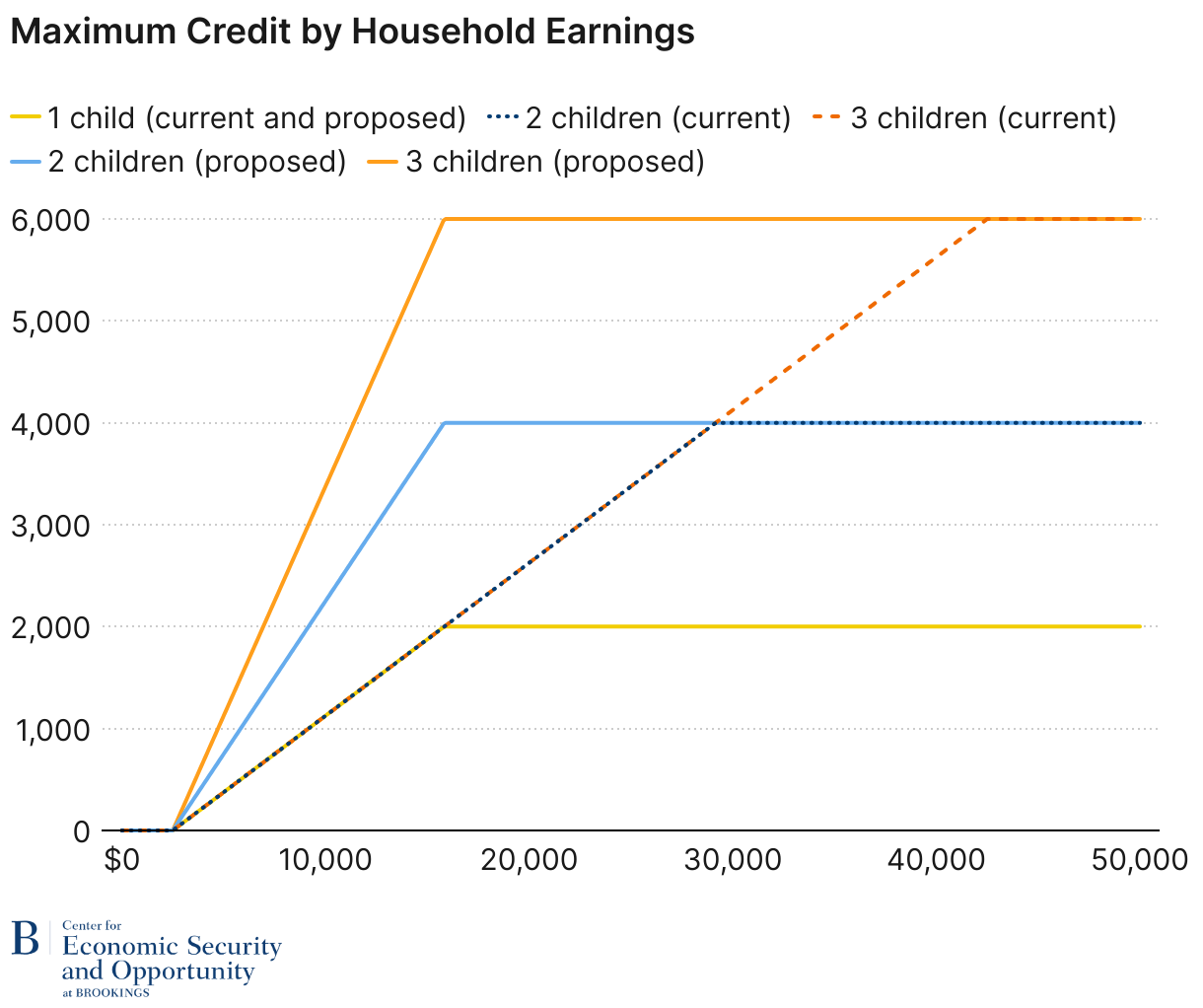

What is the proposed reform?

The framework announced this week is an expansion of the CTC, but it is far less generous to the lowest income families than the temporary expansion that was enacted for 2021.

Specifically, the reform would:

- Increase the amount of the credit that can be provided on a refundable basis from $1,600 to $1,800 in 2023, $1,900 in 2024, and $2,000 in 2025. (It would not eliminate the earnings test and phase-in—the lowest income families will still receive no support from the CTC).

- Allow a steeper phase-in for families with more than one child, so families could reach the maximum benefit per child at around $16,000 in earnings regardless of the number of children. (The amount received for most low-income families would be slightly less for 2023 and 2024, as some of the features of the deal phase in.)

- Adjust the $2,000-per-child full credit amount for inflation starting in 2024.

- Allow families to use either the prior year’s earnings or their earnings for the tax year to claim the credit.

The fight around the phase-in

Debates around the CTC reflect competing goals. Those most concerned about alleviating child poverty tend to favor full refundability and the elimination of the earnings test. Those who want to ensure parents are in the labor force prefer a structure which boosts the incentives to work by eliminating the credit for those who don’t and phasing in the credit gradually as earnings increase.

The proposed framework continues to exclude families without earnings, and full benefits remain unavailable to those with earnings around $16,000 or less, who are typically living in poverty. But the reform does boost the credit for many low-income working families with more than one child, and the prior year rule might mean that some families with intermittent earnings could access the benefits where they can’t under current law.

The Center on Budget and Policy Priorities has crunched the numbers and estimates that the proposal would increase the credit amount for about 16 million children, pulling an estimated 400,000 of them out of poverty in the first year (500,000 by 2025) and making 3 million more of them less poor. It offers much less support than the 2021 expansion, which included a larger credit and eliminated the earnings test and phase-in, pulling more than 2 million children out of poverty.

In a 2023 essay, my Brookings colleagues Wendy Edelberg and Melissa Kearney tried to strike a balance with a proposal that shared some features with a Bipartisan Policy Center proposal from 2021. Importantly, both proposals included partial benefits to those with no earnings but still maintained a phase-in to build in a work incentive. Both proposals also better targeted the CTC to low- and middle-income families by starting the phase-out for affluent families at a lower income threshold than current law.

This week’s deal presents a CTC that falls short on both of these elements. It does not help children in families without earnings. There is convincing evidence that resources in childhood make a big difference to child well-being and life trajectory, so this is a missed opportunity. A compromise CTC with partial benefits for non-earners might nudge a few parents to stay out of the labor force relative to the status quo, but that is not necessarily a bad thing for children and families. This week’s proposed reform also continues giving the credit to high-earning families—those resources going to families in the top 5 or 10% could be better utilized to expand the credit at the bottom of the income distribution.

The proposed change to the CTC would help millions of low-income children. But we are increasingly using the tax code in lieu of a traditional cash safety net. If tax credits are to be the major source of cash support for children living in poverty, this proposal does not go far enough for poor families and maintains too much support for those with higher incomes. Boosting the CTC is a good first step—let’s ensure it’s not the last.

Author

-

Acknowledgements and disclosures

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

The new Child Tax Credit deal is really a safety net deal—and by that measure it is only a start

January 18, 2024