Policymakers in Asia are rightly focused on the potential reconfiguration of global supply chains, given the implications these shifts may have for the development of their export-oriented and highly open economies. While the focus on potential shifts on the supply side of the global and regional trading system is well-justified, equally dramatic shifts on the demand side deserve as much attention. This blog provides evidence of the growing role of final demand originating from within emerging Asia and draws policy implications for the further evolution of trade integration in the region.

Trade has been a major driver of development in East Asia with Korea and Japan reaching high-income status through export-driven development strategies. Emerging economies in East Asia, today account for 17 percent of global trade in goods and services. With an average trade-to-GDP ratio of 105 percent, these emerging economies in East Asia trade a higher share of the goods and services they produce across borders than emerging economies in Latin America (73.2 percent), South Asia (61.4 percent), and Africa (73.0 percent). Only EU member states (138.0 percent), which are known to be the most deeply integrated regional trade bloc in the world, trade more. Alongside emerging East Asia’s rise in global trade, intra-regional trade—trade among economies in emerging East Asia—has expanded dramatically over the past two decades. In fact, the rise of intra-regional trade accounted for a bit more than half of total export growth in emerging East Asia in the last decade, while exports to the EU, Japan, and the United States accounted for about 30 percent, a pattern that was briefly disrupted by the COVID-19 crisis. In 2021, intra-regional trade made up about 40 percent of the region’s total trade, the highest share since 1990.

Drivers of intra-regional trade in East Asia are shifting

Initially, much of East Asia’s intra-regional trade integration was driven by rapidly growing intra-industry trade, which in turn reflected the spread of cross-border global value chains with greater vertical specialization and geographical dispersion of production processes across the region. This led to a sharp rise in trade in intermediate goods among emerging economies in Asia, while the EU, Japan, and the United States remained the main export markets for final goods. Think semiconductors and other computer parts being traded from high-wage economies, like Japan, Korea, and Taiwan, China for final assembly to lower-wage economies, initially Malaysia and China and more recently Vietnam, with final products like TV sets, computers, and cell phones being shipped to consumers in the U.S., Europe, and Japan.

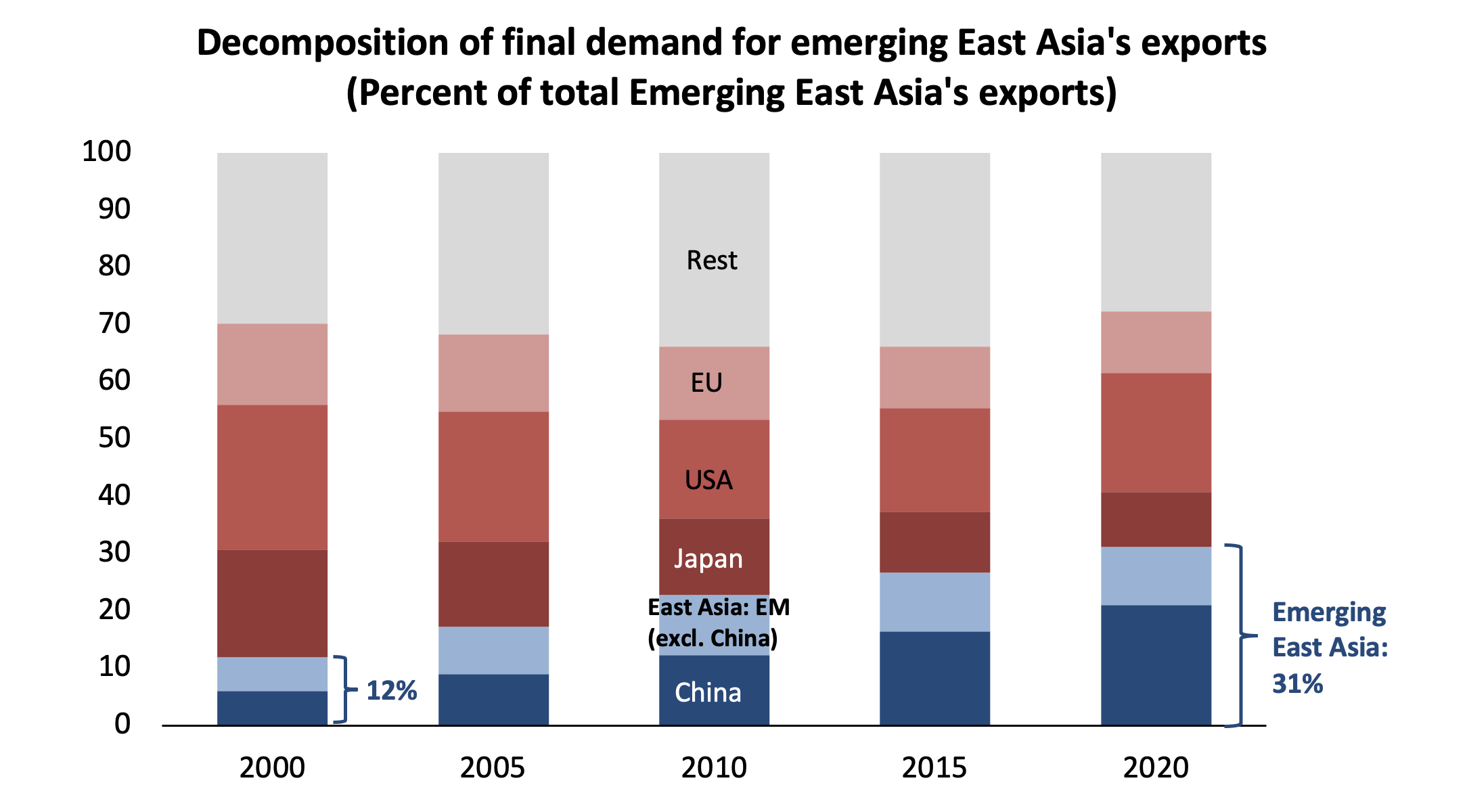

The sources of global demand have been shifting. Intra-regional trade no longer primarily reflects shifts in production patterns but is increasingly underpinned by changes in the sources of demand for exports of final goods. With rapid income and population growth, domestic demand growth in emerging East Asia has been strong in recent years, expanding by an average of 6.4 percent, annually over the past ten years, exceeding both the average GDP and trade growth during that period. China is now not only the largest trading partner of most countries in the region but also the largest source of final demand for the region, recently surpassing the U.S. and the EU. Export value-added absorbed by final demand in China climbed up from 1.6 percent of the region’s GDP in 2000 to 5.4 of GDP in 2021. At the same time, final demand from the other emerging economies in East Asia has also been on the rise, expanding from around 3 percent of GDP in 2000 to above 3.5 percent of GDP in 2021. While only about 12 cents of every $1 of export value generated by emerging economies in Asia in 2000 ultimately met consumer or investment demand within the region, today more than 30 cents meet final demand originating within emerging East Asia.

Figure 1. Destined for Asia

Source: OECD Inter-Country Input-Output (ICIO) Tables, staff estimates. Note: East Asia: EM (excl. China) refers to Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Thailand, and Vietnam.

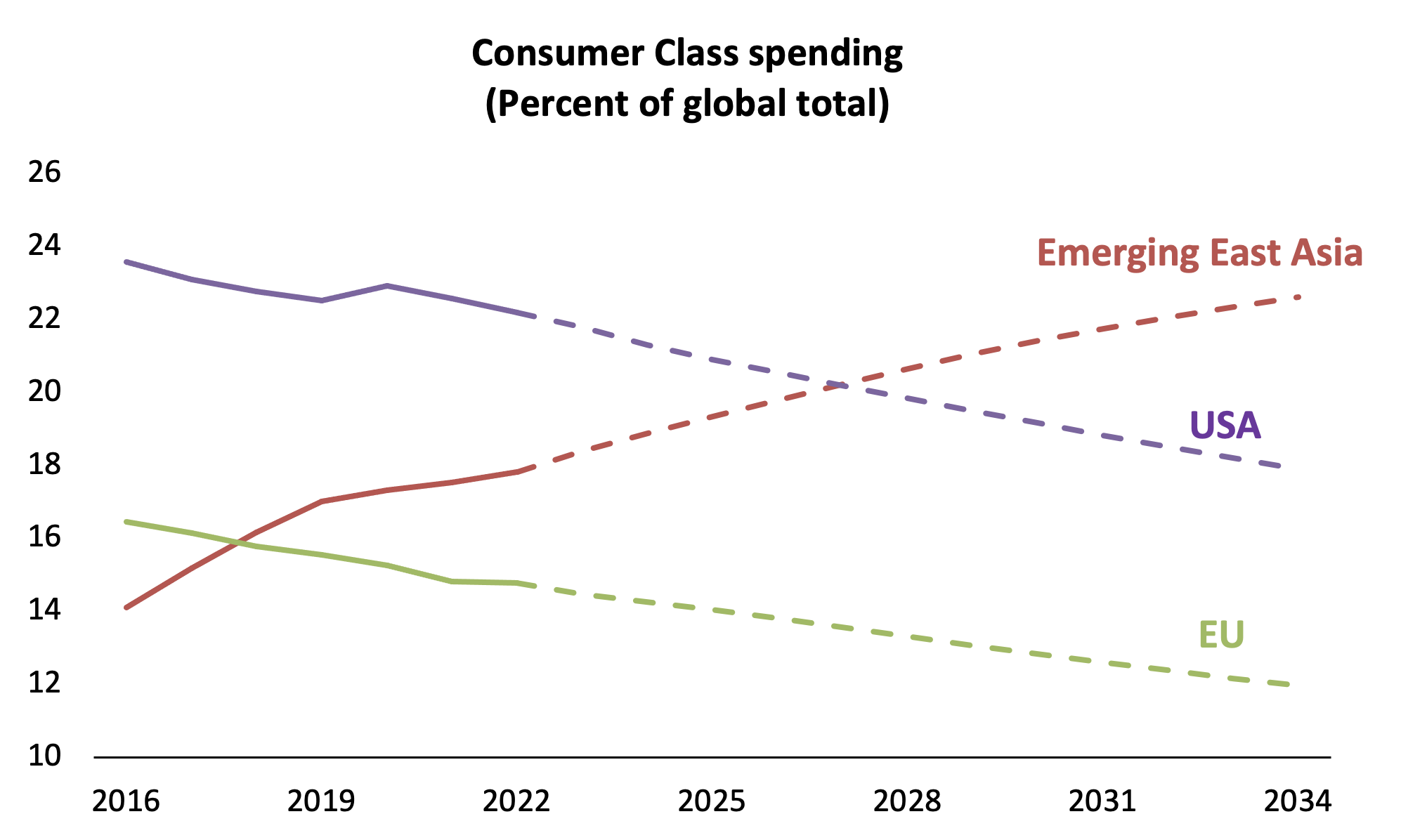

These shifting trade patterns reflect dramatic shifts in the geography and makeup of the global consumer market. Emerging East Asia’s middle class has been rising fast from 834.2 million people in 2016 to roughly 1.1 billion in 2022. Today more than half of the population—54.5 percent to be precise—has joined the ranks of the global consumer class, with daily consumer spending of $12 per day or more. According to this definition, East Asia accounted for 29.0 percent of the global consumer-class population by 2022, and by 2030 one in three members of the world’s middle class is expected to be East Asian. Meanwhile, the share of the U.S. and the EU in the global consumer class is expected to decline from 19.2 percent to 15.8 percent. If we look at consumer-class spending, emerging East Asia is expected to become home to the largest consumer market sometime in this decade, according to projections, made by Homi Kharas of the Brookings Institution and others, shown in the figure below.

Figure 2. Reshaping the geography of the global consumer market

Source: World Bank staff estimates using World Data Pro!, based on various household surveys. Note: Middle-class is defined as spending more than $12 (PPP adjusted) per day. Emerging East Asia countries included in the calculation refer to Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Thailand, Vietnam, and China.

Intraregional economic integration could act as a buffer against global uncertainties

Emerging economies in Asia are known to be the factories of the world. They play an equally important role as rapidly expanding consumer markets which are already starting to shape the next wave of intra-regional and global trade flows. Policymakers in the region should heed this trend. Domestically, policies to support jobs and household income could help bolster the role of private consumption in the steady state in some countries, mainly China, and during shocks in all countries. Externally, policies to lower barriers to regional trade could foster deeper regional integration. While average tariffs have declined and are low for most goods, various non-tariff barriers remain significant and cross-border trade in services, including in digital services remains particularly cumbersome. Multilateral trade agreements, such as ASEAN, the Comprehensive and Progressive Trans-Pacific Partnership (CPTPP), and the Regional Comprehensive Economic Partnership (RCEP) offer opportunities to address these remaining constraints. Stronger intraregional trade and economic integration can help diversify not just supply chains but also sources of demand, acting as a buffer against uncertainties in global trade and growth.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Asia’s trade at a turning point

March 20, 2023